New Brand Finance data shows the chemicals sector edges towards recovery as collective brand value rises to $83.3 billion

LONDON, 7 April 2026 – The chemicals sector enters 2026 in a fragile recovery phase, with its total brand value rising 1% to USD83.3 billion, according to the Chemicals 50 2026 report from Brand Finance, the world's leading brand valuation consultancy. Last year, the sector’s collective brand value stood at USD82.5 billion, following a decline from its 2024 performance (USD83.7 billion), as margin pressures and weaker investor sentiment weighed on performance, leaving the sector just below its previous peak.

Geopolitical developments have added a further layer of uncertainty to the sector’s outlook. Recent disruptions to global energy supply, including attacks affecting liquefied natural gas infrastructure in the Middle East in March 2026, have highlighted the vulnerability of feedstock supply chains. Against this backdrop of a fragile recovery and ongoing geopolitical uncertainty, the world’s leading chemicals brands have demonstrated resilience, supported by strong brand fundamentals and strategic execution.

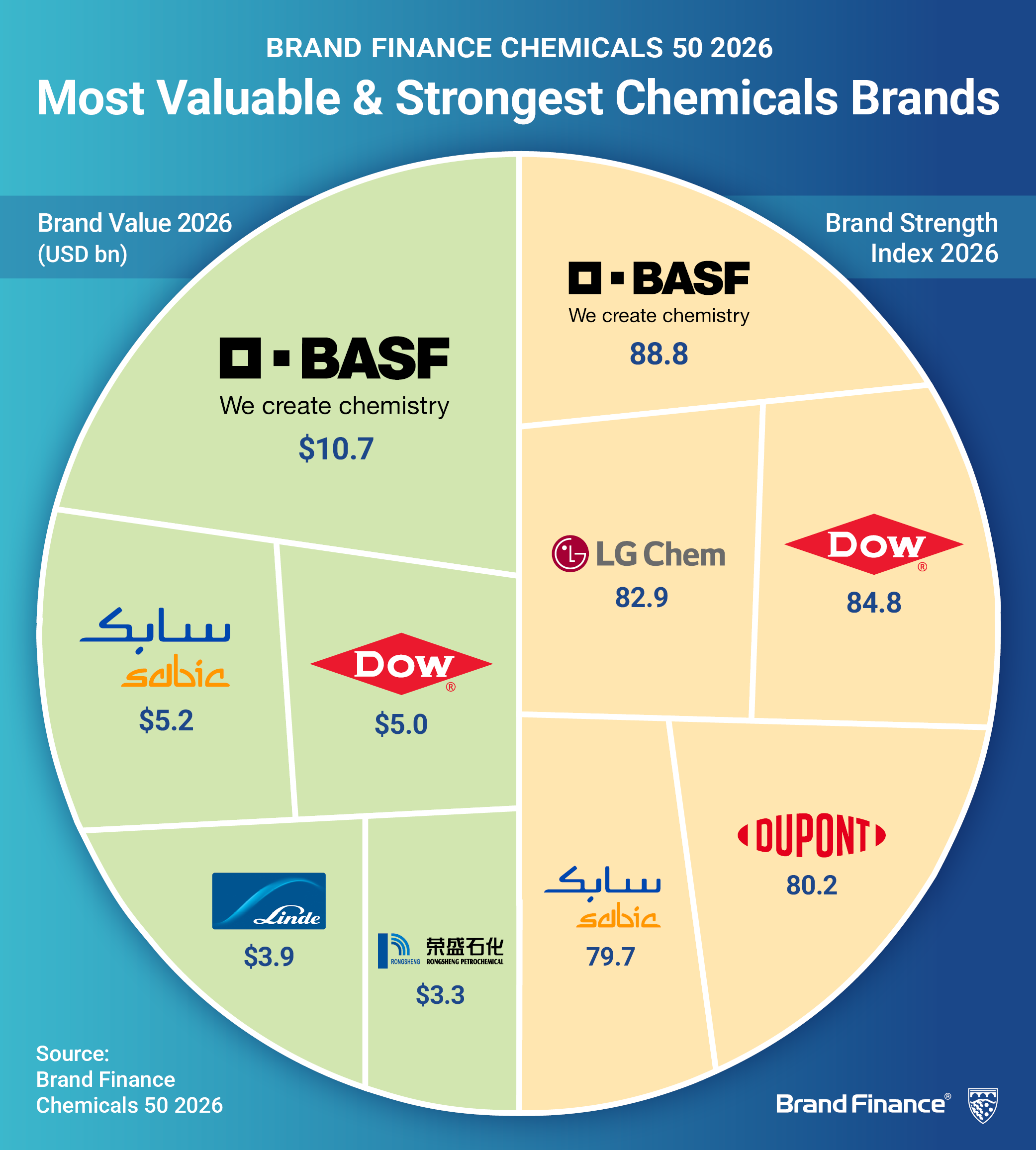

For the 12th consecutive year, BASF (brand value up 13% to USD10.7 billion) retains its position as the world’s most valuable chemicals brand. This sustained leadership reflects the brand’s resilience despite a challenging operating environment.

SABIC (brand value up 5% to USD5.2 billion) remains in second position for the sixth consecutive year, with modest growth reflecting resilience amid continued pressures in the global petrochemicals market. Early signs of stabilisation are emerging, with SABIC reporting annual revenues of SAR116.5 billion (approximately USD31 billion) in 2025, supported by higher sales volumes despite ongoing pricing pressures.

Dow (brand value up 6% to USD5 billion) retains third position, with brand value growth driven by a notable improvement in brand strength. Despite revenue pressures from declining selling prices and weaker demand in segments such as packaging and specialty plastics, Dow has strengthened its positioning through a sharper focus on specialty chemicals and targeted capacity expansion in silicones and alkoxylates in the US.

Savio D’Souza, Global Sector Head of Chemicals, Brand Finance, commented:

“The chemicals industry is in the early stages of a fundamental reorientation, from volume-driven commodity production toward innovation-led, sustainability-anchored businesses. Brand is the thread running through that transition. It's what signals credibility to customers when you're asking them to adopt new materials or processes. It's what attracts the talent and partners you need to innovate at pace. It's what gives investors' confidence in a long-term thesis. The brands rising fastest in our rankings this year aren't waiting for the cycle to turn; they're building the assets that will make them indispensable when it does."

Nutrien (brand value up 22% to USD2.6 billion) has emerged as the fastest-growing chemicals brand in 2026, recording the largest brand value increase across the sector. This performance is largely driven by improvements in its brand strength with Brand Strength Index (BSI) score of 71.8/100 (2026) from 66.6/100 in 2025, with Nutrien achieving notable gains in credibility, appeal, and overall reputation across key markets including Canada, US, and Australia.

Morocco's national phosphate champion, OCP Group (brand value at USD603 million) is a new entrant this year, securing the 50th position and standing out as a brand to watch in the global chemicals sector. The brand’s strong debut is supported by rising global demand for phosphate-based fertilisers and the company’s continued investment in expanding production capacity and strengthening its international footprint. OCP controls between 68 and 70% of the world's phosphate rock reserves and holds a 31% share of the global phosphate product market.

BASF rises from third place to become the strongest chemicals brand in 2026, achieving a Brand Strength Index (BSI) score of 89/100 and an AAA brand strength rating, driven by strong B2B performance, high trust among industrial partners, and robust scores across reliability, reputation, and engagement in key markets including Germany, Japan, and South Korea, alongside continued investment in sustainable innovation.

Dow climbs from eighth to second strongest, with a BSI score of 85/100 and an AAA brand strength rating, supported by strong perceptions of credibility, knowledge, appeal, price acceptance, and recommendation, particularly among industrial customers in China, India, and South Korea.

Meanwhile, LG Chem (brand value up 7% to USD2.5 billion) moves from fourth to third place, achieving a BSI score of 82.9/100 and an AAA- rating, with improved performance across credibility, reliability, and appeal, supported by strong domestic familiarity and continued investment in battery materials, sustainable polymers, and next-generation technologies.

Beyond the core Chemicals 50 ranking, Brand Finance also evaluates adjacent segments within the broader chemicals' ecosystem, highlighting continued resilience and leadership across specialised categories.

In the paints and coatings sector, Sherwin-Williams (brand value up 7% to USD9.1 billion) retains its position as the most valuable brand for the fifth consecutive year. Despite a decline in brand value, Asian Paints (brand value down 13% to USD1.4 billion) remains the strongest brand in the segment, achieving a BSI score of 86.8/100 and maintaining an AAA brand strength rating, supported by exceptionally strong familiarity, reputation, and customer advocacy in its home market of India.

In the agri-nutrients segment, Nutrien (brand value up 22% to USD2.6 billion) continues to lead as the most valuable brand, underpinned by consistent execution of its strategy focused on operational excellence, disciplined capital allocation, and business simplification. Strong scores in credibility and appeal across Canada, the US, and Australia have also positioned Nutrien as the strongest brand in the segment, with a BSI score of 71.8/100 and an AA brand strength rating.

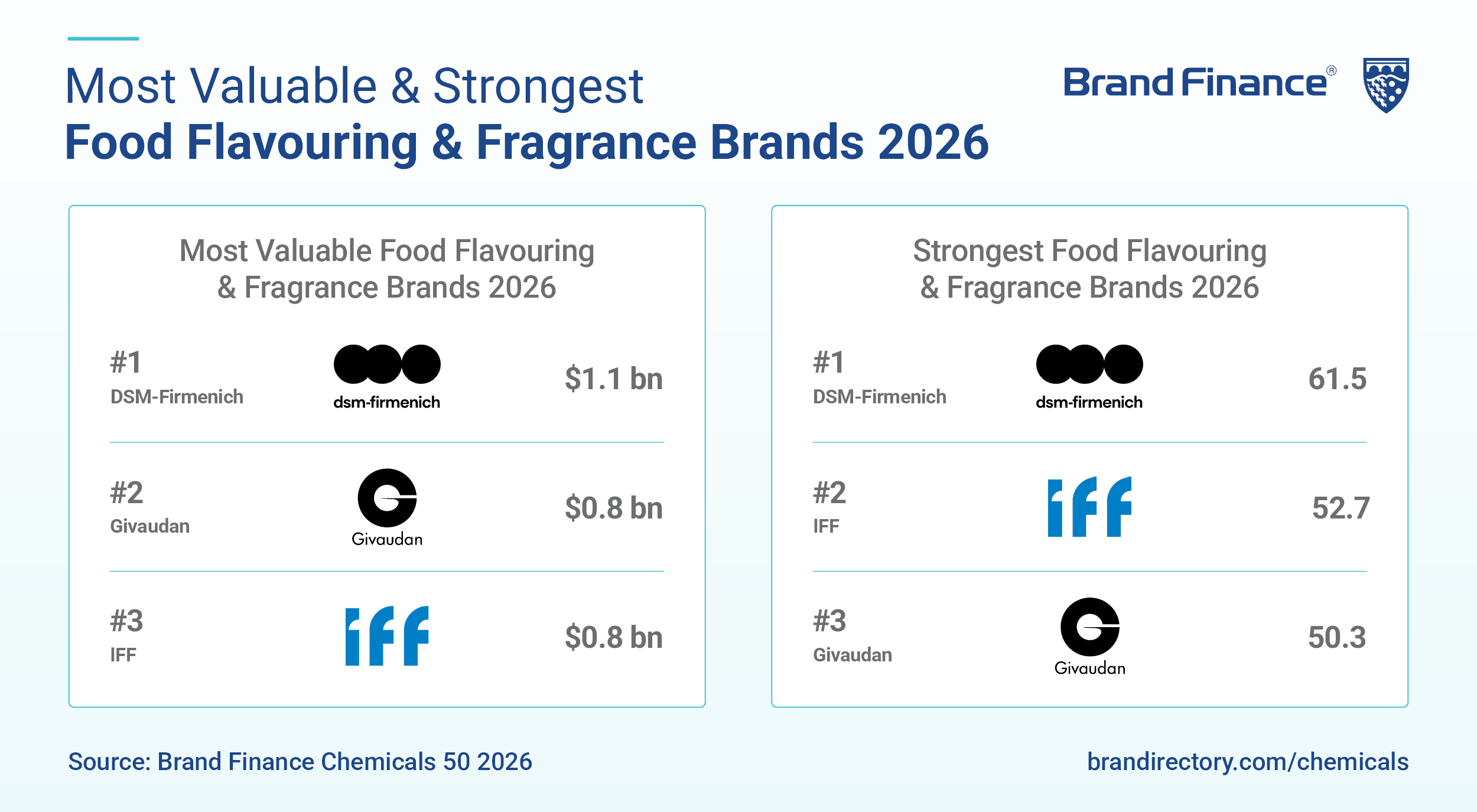

Reflecting the growing strategic importance of food flavouring and fragrance, Brand Finance has introduced a dedicated ranking for the first time, with DSM-Firmenich emerging as both the most valuable and strongest brand in the segment. With a brand value of USD1.1 billion and a BSI score of 61.5/100, the brand benefits from strong global positioning across nutrition, health, and sensory innovation.

Similarly, within the industrial gases segment, Linde (brand value at USD3.9 billion) ranks as both the most valuable and strongest brand. Stable sales of around USD33 billion in 2025, alongside growth in net income and earnings per share, reflect disciplined pricing, productivity gains, and effective cost management. Strong performance across reputation, positive contribution, and engagement in key markets such as the US and Germany further reinforces its leadership, with a BSI score of 69.1/100.

The agriscience segment remains a critical pillar of the chemicals industry with Bayer Crop Science (brand value at USD3.5 billion) retaining its position as the most valuable agriscience brand with a BSI score of 83/100, continuing to account for the largest share of Bayer’s overall brand value.

Despite broader headwinds in the global agriculture markets, the segment demonstrated resilience, achieving 5% year-on-year growth. However, in terms of brand strength, BASF Agricultural Solutions has overtaken Bayer to become the strongest agriscience brand, achieving a BSI score of 89.1/100. This shift reflects BASF’s disciplined execution across key drivers such as reliability, innovation delivery, and farmer engagement, enabling it to edge ahead in an increasingly competitive and cost-sensitive market.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.