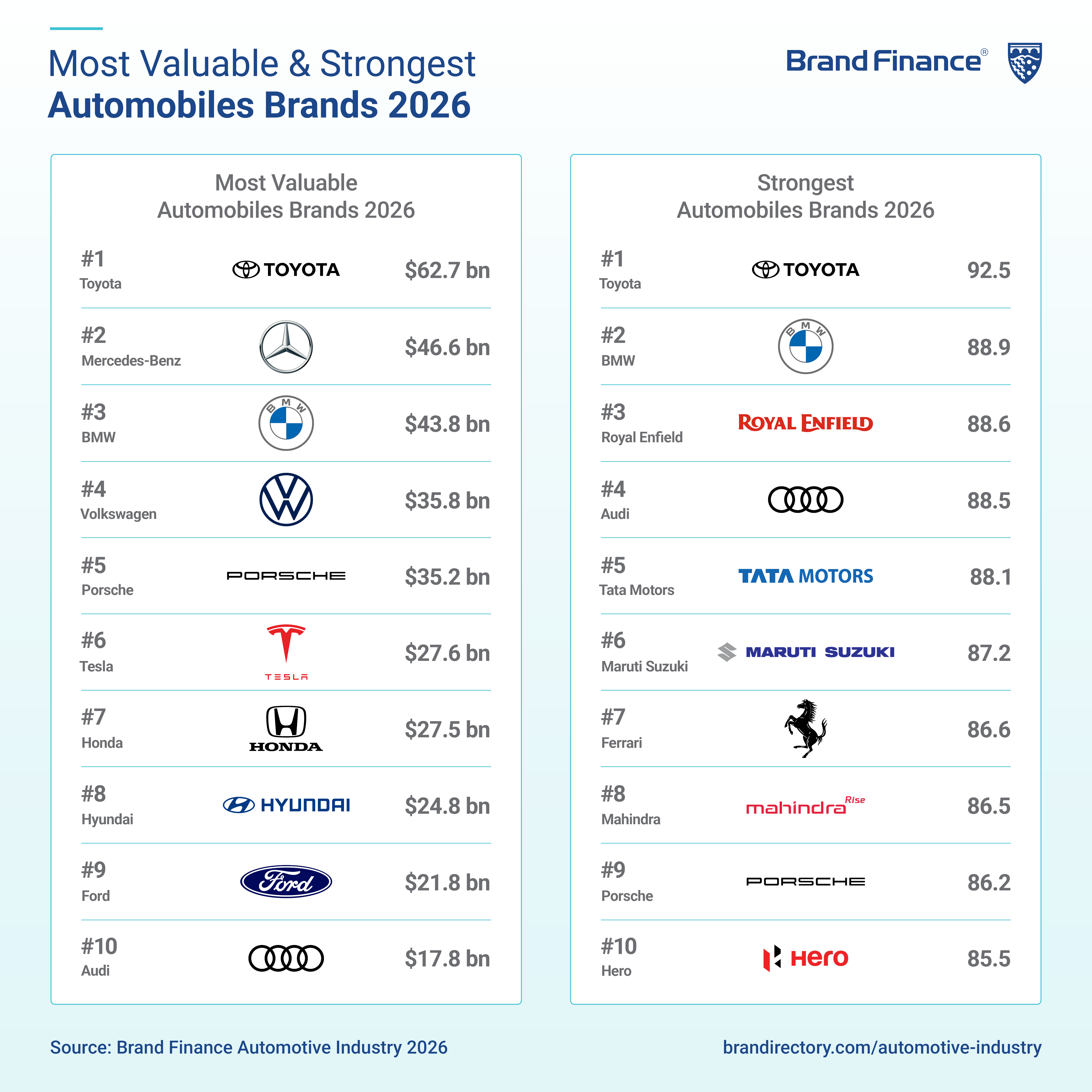

New Brand Finance data shows the sector’s collective brand value stands at $575.4 billion

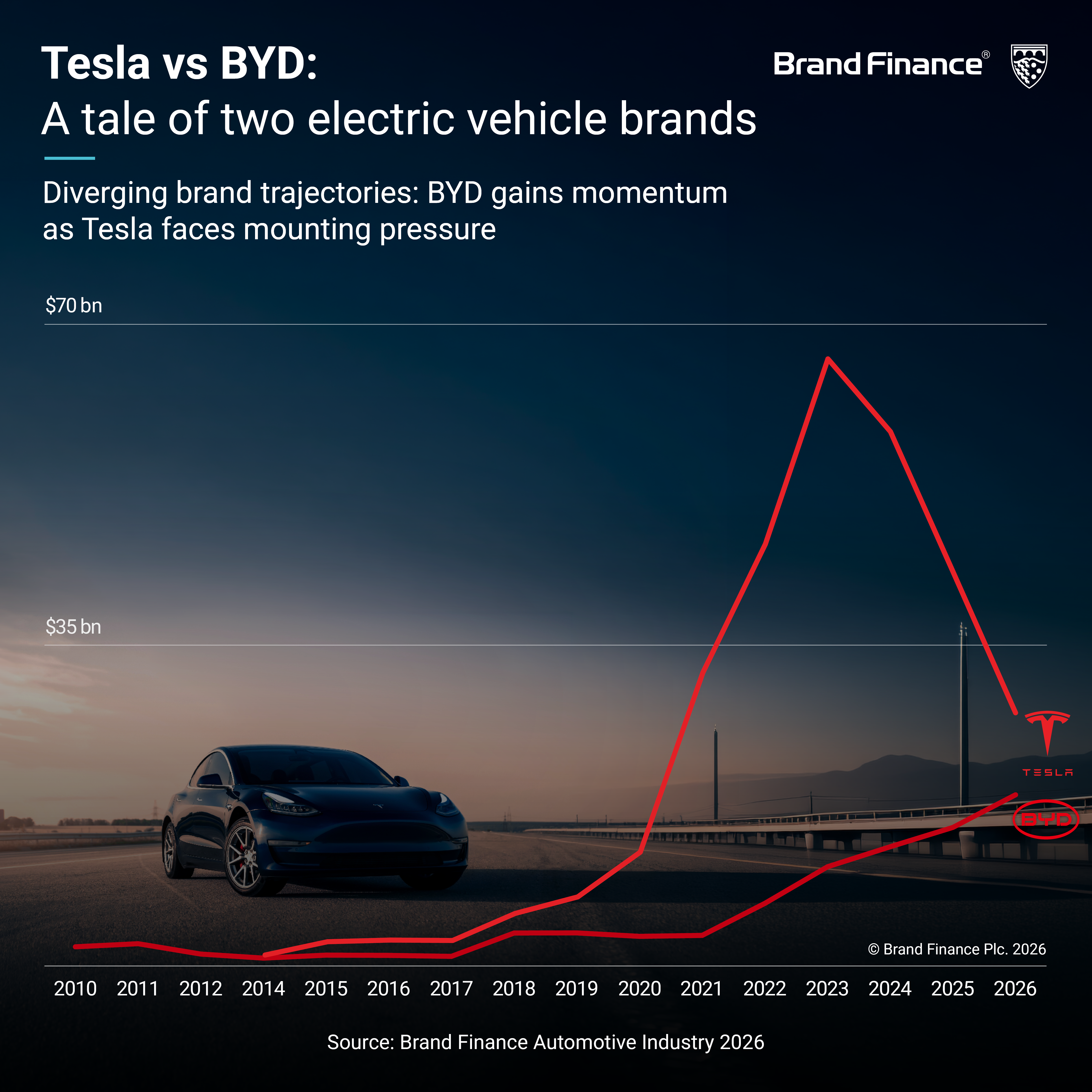

BEIJING, 23 April 2026 – The balance of power in global electric mobility is shifting, and BYD is emerging as one of its key beneficiaries. The automaker’s brand value climbed 23% to USD17.3 billion this year, lifting it to rank as the 11th most valuable automobile brand globally. In addition, its brand strength rating improved to AA+, driven by scale, affordability and growing consumer confidence, according to the Automotive Industry 2026 report from Brand Finance, the world’s leading brand valuation consultancy.

BYD’s momentum is underpinned by strong operational and financial performance, as the company has reported rising profits on the back of robust global EV sales supported by its ability to scale production efficiently while maintaining competitive pricing.

Meanwhile, Zhejiang Leapmotor Technology (brand value up 67% to USD1 billion) emerges as the fastest-growing automobile brand of the year. Its rapid rise reflects accelerating momentum within China’s highly competitive EV market, as well as growing relevance in the broader global automotive landscape.

The brand’s performance has been underpinned by a series of decisive product and technology-led initiatives throughout 2025. Central to this growth was the launch of multiple new models built on Leapmotor’s LEAP 3.5 architecture, including the B10, B01 and D19.

Geely (brand value up 26% to USD4.5 billion) further reinforces China's collective strength, driven by a surge in New Energy Vehicle (NEV) sales, the deepening of its One Geely integration strategy, and accelerated global market expansion. The collaboration between Geely Auto, Lynk & Co, and Zeekr under this unified strategy unlocked greater operational efficiencies across research and development, manufacturing, and supply chains, helping maintain gross profit margins despite competitive price pressures. NEV sales, encompassing both Battery Electric Vehicles and Plug-in Hybrids, recorded a notable 126% year-on-year increase in the first half of 2025, significantly outpacing overall market growth.

Another strong showing is by AITO (new entrant, brand value at USD3.4 billion), debuting on the global stage as the 28th most valuable brand in the sector. Adhering to its brand philosophy of ‘Intelligence Redefining Luxury’, Aito surpassed one million cumulative users and established itself as the best-selling Chinese luxury car brand in the domestic market in 2025, signalling that Chinese brands are now competing credibly at the premium end of the global automotive spectrum.

Scott Chen, Managing Director China, Brand Finance, commented:

“China's automotive brands have moved well beyond their domestic roots as this year’s rankings tell a story of an industry that has matured rapidly. Chinese brands now competing credibly at every level of the global automotive market and the challenge ahead is not scale, which China has already achieved, but sustained brand strength in international markets. Brands that invest in perception, trust, and consumer engagement beyond China will be the ones that define the next decade of global automotive."

China's automotive sector brand presence in the 2026 rankings span the full spectrum of the industry. Premium and intelligent mobility challengers Changan (brand value down 5% to USD2.4 billion), Xpeng (brand value up 65% to USD2 billion), Li Auto (brand value down 29% to USD1.9 billion), NIO (brand value up 5% to USD1.9 billion), and LYNK&CO (brand value up 30% to USD1 billion) continue to strengthen their global footprint.

Established domestic powerhouses anchor the rankings with scale and breadth across China's vast passenger vehicle market. Haval (brand value down 15% to USD2.1 billion), Han (brand value down 2% to USD2.0 billion), Song (brand value down 3% to USD1.6 billion), Tang (brand value down 10% to USD1.2 billion), Great Wall (brand value down 9% to USD1 billion), Wuling (brand value up 4% to USD591 million), Yuan (brand value down 21% to USD686 million), Qin (brand value down 33% to USD581 million), and GAC (brand value down 22% to USD528 million) reflect the depth of China's domestic market presence, though intensifying competition and pricing pressure weighed on several brands within this segment.

Beyond passenger vehicles, China's commercial and specialist vehicle brands reinforce the country's unrivalled industrial strength. Dongfeng (brand value up 18% to USD1.2 billion), FAW Jiefang (brand value down 17% to USD1.2 billion), and Sinotruk (brand value up 1% to USD1.2 billion) lead the tier, followed by JAC Motors (brand value down 16% to USD750 million), Yutong (brand value down 17% to USD743 million), and Loncin Motor (brand value up 38% to USD663 million).

While China's brands continue to gain ground, the broader global picture remains challenging. The automobile sector recorded consecutive declines, falling 1% in 2025 and a further 7% in 2026, with total brand value now standing at USD575.4 billion. Concerns around charging infrastructure, battery durability, and upfront costs have tempered consumer confidence globally, and manufacturers that invested aggressively in electrification are facing excess inventories and margin compression. It is precisely in this environment that the agility and competitive pricing of Chinese brands have proven most advantageous.

Beyond vehicle manufacturers, Brand Finance is also releasing new insights into the auto components sector, where Weichai (brand value down 1% to USD2.9 billion) ranks sixthand Hasco (brand value down 5% to USD2.1 billion) at ninth. Fuyao Glass Industry (new entrant, brand value at USD1.2 billion) made a debut into the global ranking at 18th this year.

Meanwhile, for the mobility sector, CaoCao (new entrant, brand value at USD1.3 billion) enters the global ranking at 14th, marking a significant milestone for China's shared mobility industry. The company now operates in 195 cities across China and reported a revenue of USD2.9 billion in 2026, up 38% year on year compared to 2025.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.