This article was originally published in the Brand Finance Insurance 100 2026.

The insurance sector is entering a period of structural change in how brands create and sustain value. AI-driven disruption, macroeconomic uncertainty, and evolving financial reporting standards are reshaping not only how insurers operate, but how they are perceived by customers, investors, and the market more broadly.

AI and the compression of distribution

Insurance distribution has already undergone one major transformation through digital comparison platforms such as MoneySuperMarket. These platforms increased transparency and reduced switching costs, shifting competition toward price and

efficiency.

Generative AI represents a second and more structural wave of disruption

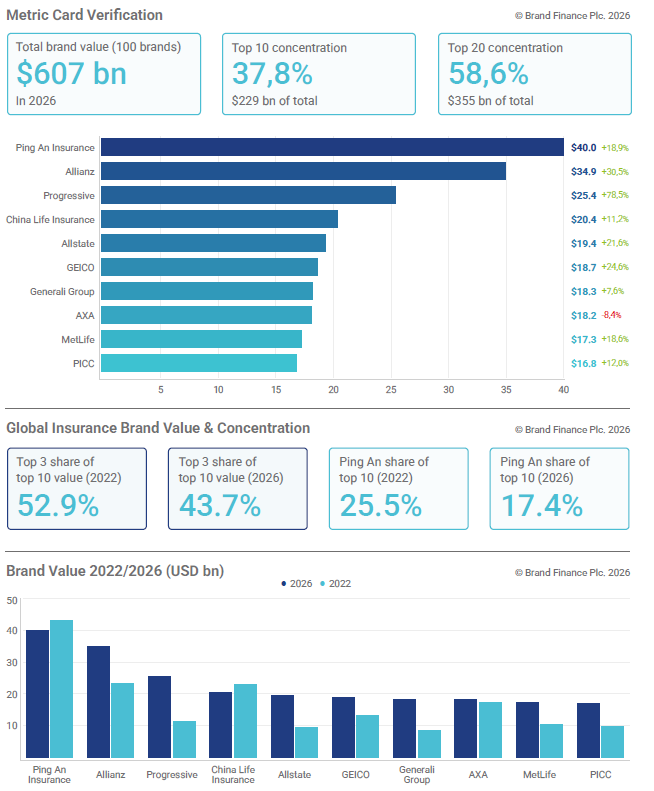

For instance, Allianz, the world's second-ranked insurance brand in 2026, grew its brand value by 31% to USD34.9 billion, while Zurich recorded 27% growth to USD12.9 billion and Ping An Insurance, the sector's highest-valued brand, expanded by 19% to USD40.0 billion. Collectively, these three brands alone added over USD17 billion in combined brand value year-on-year. This clear commercial growth highlights that while accounting reporting structures fluctuate under new standards, the core marketplace strength and long-term value of leading insurance brands remain firmly intact.

What distinguishes AI from previous distribution layers is its ability to compress the decision-making process. Rather than presenting a broad set of options, AI tools may reduce choice to a shortlist or even a single recommendation fundamentally altering how brands compete.

This shift is particularly important when viewed alongside the Insurance 100 2026 ranking, which already highlights a concentrated market structure. The top 10 insurance brands account for approximately 36% of total brand value, reflecting their dominance in awareness, trust, and scale.

As AI narrows the consideration set, this concentration is likely to increase, reinforcing the position of leading brands while reducing visibility for others. In this environment, brand strength operates on two distinct levels. The first is familiar: strong brands command direct consumer loyalty, enabling insurers to retain customers, sustain pricing power, and reduce dependence on intermediaries.

The second is emerging and less well understood: the ability to communicate a compelling value proposition to the AI-driven systems now shaping customer choices.

For AI-driven systems, the signals are different. In addition to brand awareness or advertising presence, what matters is the quality and consistency of information that AI tools can draw on: online reviews and aggregate ratings, clear and structured product information, intermediary assessments, and the depth of trust signals across digital touchpoints.

Insurers that perform well on these dimensions are more likely to be surfaced and recommended, undermining the benefit of historic scale. The top 3 share of the pool actually fell from 52.9% to 43.7%, because the total pool grew by USD61 billion and

mid-tier brands caught up. However, the gap in absolute value between the top brands and the rest still widened: Progressive tripled its value while bottom-half brands grew more modestly.

The insurance brand race: Digital readiness is the new dividing line

Five years ago, the global insurance rankings looked largely settled. Ping An sat comfortably at the top, a handful of European giants held the middle ground, and American insurers occupied a broad, unremarkable tier below them. By 2026, that picture

has shifted in ways that reward a closer look, because the brands that moved are telling a clear story about where the industry is heading.

The more revealing measure is the absolute gap. Ping An's brand value of USD40 billion is now roughly 2.4 times that of PICC at rank 10. The leaders are not squeezing out the competition in relative terms they are simply outrunning them in absolute ones. The

distance between first and tenth is growing even as the percentage math softens.

Three brands that moved and why

Progressive is the decade's most striking insurance brand story. Ranked eighth in 2022, it sits third today, with a brand value that has more than doubled. The engine behind that climb is not advertising spend or market consolidation; it is data. Progressive's Snapshot telematics programme now draws on 14 billion miles of real driving behaviour, feeding machine learning models that price risk 9% more accurately than traditional methods.

AI-assisted photo estimation tools have enabled adjusters to handle 2.5 times their previous claims volume. The result is a combined ratio of 86.0, among the best in the industry and a business that increasingly resembles a real-time data platform with an

insurance license.

Generali's nine-place climb from rank 16th to seventh is less discussed but equally significant. Its "Lifetime Partner 24" strategy repositioned the Italian giant around prevention rather than protection health wearables, IoT home sensors, digital direct sales adding 115% to its brand value in the process. It is a reminder that digital transformation does not require being a tech company; it requires building the customer relationships that technology makes possible.

Ping An's story is different again. Its brand value edged down slightly in dollar terms, but that headline obscures something more important. In 2024 alone, its AI systems handled 1.8 billion customer service interactions 80% of all contact volume. Net profit surged 48%. The company now holds over 55,000 patent applications globally and ranks second worldwide in generative AI patents. Ping An is not growing its brand value only through marketing; it is building a technological infrastructure that competitors will take years to replicate.

The insurance rankings of 2030 are likely being determined today, in decisions about AI investment, telematics infrastructure, and digital claims experience. The brands that moved fastest between 2022 and 2026 did so not by acquiring competitors or entering new markets, but by changing what insurance fundamentally does from a reactive, demographic-based product into a dynamic, behavior-responsive service.

UK focus: Portfolio strategies and brand architecture efficiency

The UK insurance market offers a clear illustration of how these dynamics may play out.

Historically, insurers such as Aviva have adopted multi-brand portfolio strategies to maximize presence across comparison platforms, target different customer segments, and increase overall share of consideration. In a model where visibility drives choice, this approach has been effective in capturing incremental demand.

However, AI-led distribution challenges this logic. If AI tools reduce customer choice to a limited number of recommendations, the advantage of maintaining multiple brands within the same portfolio may diminish. Rather than increasing “shelf space,” additional brands may compete with one another for inclusion in algorithmic outputs, limiting their incremental contribution to overall brand value.

This raises important questions about brand architecture efficiency. Insurers need to reassess whether maintaining multiple overlapping brands continues to deliver value, or whether greater emphasis should be placed on strengthening a smaller number of highly distinctive master brands. In an AI-driven environment, depth of brand equity may become more valuable than breadth of brand presence.

Geopolitical and financial risk: Brand as a stability multiplier

Alongside technological disruption, insurers are operating in an increasingly uncertain macroeconomic and geopolitical environment.

Ongoing conflicts, inflationary pressures, and financial market volatility are contributing to heightened risk across underwriting and investment performance. These conditions not only impact financial outcomes but also influence how customers and investors evaluate insurers.

In this context, brand plays a critical role as a signal of stability and resilience. Stronger brands are better positioned to retain

customers during periods of uncertainty, support pricing discipline, and maintain investor confidence.

In sectors such as insurance where long-term commitments and financial security are central, trust becomes a key driver of both demand and valuation.

As a result, brand strength increasingly functions as a risk mitigator, helping to stabilise revenues and support long-term growth expectations in volatile conditions.

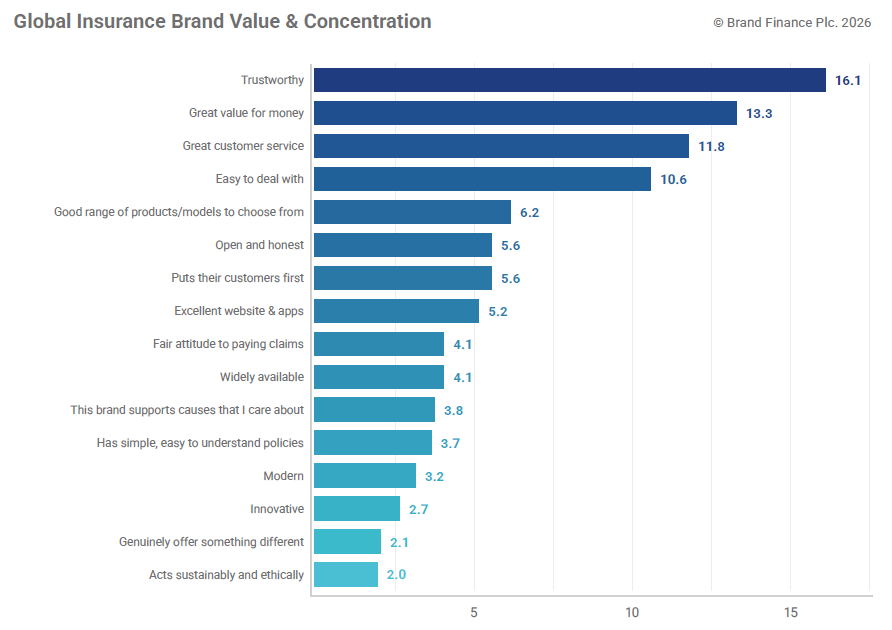

When customers choose an insurer – or decide whether to stay with one – what actually moves the needle? Brand Finance's 2026 brand equity research surveyed consumer perceptions across the global insurance sector, and the answer is clear: trust leads,

with great value for money and strong customer service a close second and third.

Trustworthiness scores 16.1, making it the single most important driver of brand equity more than 20% ahead of great value for money (13.3) in second place. Together with great customer service (11.8) and ease of dealing with (10.6), these four attributes alone account for over half of all measured driver importance.

The message is straightforward: the fundamentals of the category still dominate and in a world where AI is increasingly doing the shortlisting for customers, they will matter even more.

Further down the rankings, digital capability excellent website and apps scores 5.2, up from 3.0% in 2022. While more customers value it today, it has become a basic expectation rather than a source of competitive advantage. Customers now expect websites and apps to work well, but this alone is no longer enough to set a brand apart.

At the foot of the table, purpose-driven attributes such as sustainability (2.0), innovation (2.7), and supporting social causes (3.8) score the lowest of all. These factors matter for reputation and investor relations, but they are not yet moving consumer brand preference in insurance. For insurers, the strategic priority is clear: trust and service fundamentals first and everything else follows.

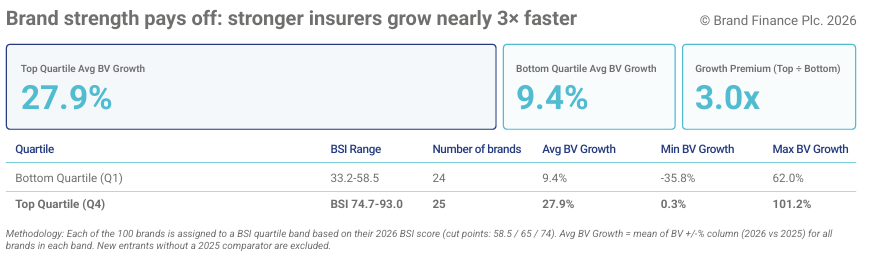

The relationship between brand strength and brand value growth is unambiguous in this year's data. Insurers in the top quartile of Brand Strength Index (BSI) scores delivered average brand value growth of 27.9% nearly three times the 9.4% recorded by brands in the bottom quartile. The gap underlines a consistent finding across Brand Finance research: brand strength is not merely a perception metric, but a leading indicator of financial outperformance.

Combining the two middle quartiles tells an equally consistent story. Brands in the mid-range of BSI performance averaged 15.9% growth sitting squarely between the two extremes and reinforcing the same directional finding: the stronger the brand, the faster it grows. The 3 times growth premium between the top and bottom quartile is the headline figure, but the broader pattern across all four bands makes the case just as powerfully.

For brands in the bottom quartile, the data presents both a challenge and an opportunity. Closing the gap on the core drivers of brand strength; trust, service quality, and customer experience has a measurable and material impact on brand value over time. Those that invest in brand building are not simply managing reputation; they are compounding a financial asset.