This article was originally published in the Brand Finance Banking 500 2025 report

The Asia & Pacific (APAC) banking sector continues to show remarkable resilience and progress in 2025, supported by an 11% year-on-year growth compared to the past year. The world’s 500 most valuable banking brands this year comprise of 183 from the region and collectively, their brand value accounts for USD721.8 billion.

While the number of APAC brands in the rankings declined slightly compared to 2024, the remarkable growth among the highest-value brands has been a key driver behind the region’s success story. Most notably, among the top 12 APAC banks in this year’s ranking, 11 experienced an average 30% increase in value while only one, Bank of Communications, recorded a decline. This trend is indicative of the region’s on-going growth trajectory as APAC banks continue to expand their market presence and strengthen their brand equity.

BANKING POWERHOUSES RISE: CHINA, INDIA, AND JAPAN STRENGTHEN GLOBAL PRESENCE

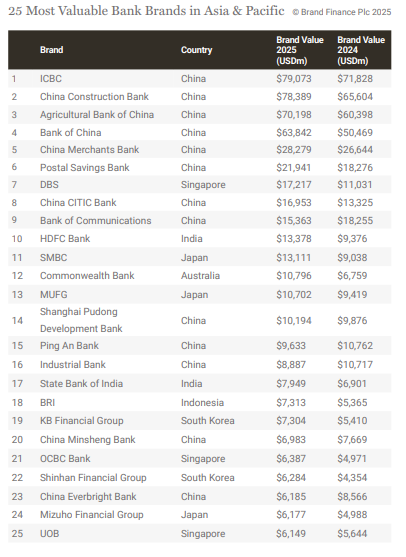

China’s growing prominence in the global banking sector is undeniable with 70 banking brands from the country making it to the Banking 500 list this year, representing 29% or USD476.5 billion of the sector’s global brand value. In comparison with the United States, 73 American brands account for 22% of the global banking brand value.

The top five Chinese banking brands in the global rankings have achieved an impressive collective brand value of USD319.8 billion—double the value of their top five US counterparts — with most of these banks being state-owned.

Asia & Pacific Banking Giants Thrive Amid Rapid Growth and Innovation Their success is largely driven by state support, allowing the banks to align their strategies with national economic priorities, including large infrastructure projects, the Belt and Road Initiative, and real estate development, all contributing to their rapid growth.

China’s ICBC holds the top spot as the world’s most valuable banking brand with a value of USD79.1 billion, reflecting a 10% increase from the previous year. This is followed by China Construction Bank and Agricultural Bank of China.

As among the world’s fastest growing country economically, India’s banking brands account for USD43 billion in value this year, represented by a total of 18 brands in the rankings. HDFC Bank stands out with a brand value of USD13.4 billion, under the leadership of Sashi Jagdishan, who ranks first among brand guardians in the global banking industry this year. He has been instrumental in steering the merger of HDFC Bank with its parent company, HDFC. Meanwhile, State Bank of India and ICICI Bank follow closely, highlighting the country’s rising prominence.

Japan, with 21 banking brands collectively valued at USD42 billion in the global rankings, takes the lead with SMBC (brand value up 45% to USD13.1 billion). This growth follows its rebranding in 2018 from SMFG, which has proven successful, delivering strong returns through synergies. MUFG and Mizuho Financial Group follow as the second and third most valuable Japanese banking brands this year.

PHILIPPINES, SINGAPORE, AND INDONESIA: STANDOUT PERFORMERS

This year, the Philippines stands out with its banking sector recording a remarkable 49% year-on-year or growth of USD3.6 billion.

A significant portion of this growth is attributed to the top two brands, BDO (brand value up 48% to USD3.7 billion) and Bank of the Philippine Islands (brand value up 53% to USD2.3 billion). With a 41% year-on-year growth, equivalent to USD9 billion among its banking brands this year, Singapore continues to contribute towards the region’s success. DBS led this growth with a notable surge of 56% to reach a brand value of USD17.2 billion, followed by OCBC Bank with 28% growth while the debutant from the island nation this year is Bank of Singapore.

This year, Indonesia's banking sector is another noteworthy success story with a 31% year-on-year growth or an increase of USD4.9 billion. Much of this growth was driven by the top three banks from the country namely, BRI (brand value up 36% to USD7.3 billion), Bank Mandiri (brand value up 52% to USD5.6 billion), and BCA (brand value up 42% to USD4.4 billion), underscoring the market's key developments.

STRENGTH IN STRATEGY

Clinching the recognition of the world’s strongest banking brand of 2025 is once again Indonesia’s BCA, with a Brand Strength Index (BSI) score of 97.1 out of 100. BCA has held on to this prestigious rank for two years consecutively, a testament to the fact that customers consistently choose BCA over its competitors, reinforcing its strong position in the market. The bank’s strategic focus on simplifying banking services, combined with strong relationships with small and medium-sized enterprises, has contributed significantly to its success. These efforts have fostered long-term partnerships and reinforced BCA’s position as a model for other banks seeking to enhance their brand strength.

The world’s top five strongest banking brands also includes Vietcombank and Bank of Singapore, each leading with a strong BSI score of 95.3 and 94.7 out of 100 respectively.

Brand Finance research has found that Vietcombank, Vietnam’s largest commercial bank, has a high level of brand familiarity within the country. Similarly, the Bank of Singapore also benefits from a high level of familiarity in its home market contributing to an increased BSI score.

These banks demonstrate that by focusing on simplifying services, strengthening customer relationships, and excelling in key brand metrics, institutions can build long-lasting customer loyalty. Their success highlights the importance of aligning brand strategies with evolving consumer needs to maintain a competitive edge.

NAVIGATING CONSUMER BEHAVIOUR AND THE DIGITAL REVOLUTION IN ASIA & PACIFIC (APAC)

Consumer behaviours across APAC are shaped by both economic and cultural factors. In developed markets like Japan, South Korea, and Australia, customers expect a blend of traditional services and digital solutions, with a focus on convenience irrespective of touchpoint, through branch networks and mobile apps.

In China, rapid digital transformation has made mobile banking and digital wallets essential for customer loyalty, while mainland Asia adopts a hybrid approach, blending fintech with physical branches for a more personalised experience.

South Korea provides a striking example of technology reshaping banking, with KB Financial Group’s KB Star Banking app, which integrates key banking services and features such as the KB Wallet. The 2025 study is following a surge in engagement, after the app reached 12 million monthly users in 2023, according to the bank’s annual report.

Mobile banking and digital platforms continue to rise in importance both in APAC and around the world. This is particularly true in China and India, as mobile banking has become a daily necessity, while markets like Singapore and Hong Kong integrate multi-channel experiences, blending technology with in-branch services.

AI adoption is rising across the region, improving efficiency and reducing wait times, as demonstrated by the Commonwealth Bank of Australia’s investment in AI. Malaysia’s Maybank in the other hand, leverages digitalisation through its M25+ plan to drive growth and embrace sustainable practices, positioning itself as a catalyst in the region’s digital transformation.

Looking ahead, the region’s banking brands are set to expand their influence by balancing local strengths with strategic innovation. Their deep market understanding, strong government ties, and extensive branch networks provide resilience amid geopolitical uncertainty and high interest rates, allowing them to source funds efficiently.

At the same time, leading banks are driving growth through digitalisation, preparing for climate-related challenges, and excelling in specialised sectors. By combining these advantages, APAC banks are well-positioned to shape the future of global finance.

To remain competitive within the region, banking brands must focus on key strategies that blend a thorough understanding of local markets with a commitment to digital transformation. By embracing customer-centric technologies, banks can elevate their service offerings while effectively addressing emerging challenges.

Building strong brand partnerships and ensuring compliance with regulatory standards will be crucial to maintaining relevance in an increasingly dynamic environment. The most successful banking brands in this region will be those capable of navigating complex market dynamics with agility and strategic foresight, ensuring that their institutions not only adapt to the evolving global financial landscape but also meet the ever-changing demands of consumers.