This article was originally published in the Brand Finance Tyres 25 Report 2026.

Analysis from the Brand Finance Global Brand Equity Monitor, November 2025 - Europe (UK, Spain, Italy, Germany, Austria, France, Switzerland) and UK only

Head of Sports Services,

Brand Finance

Tyre is a category that lives or dies on salience. When a motorist needs a new set of tyres, often urgently, often reluctantly, the brand that springs to mind first wins the sale. In other words, when you go to the tyre retailer and various brands are shown within a particular price range, you more often than not select the one that you know. That makes football, the most-watched sport across Europe and the UK, an almost ideal salience engine. Roughly half of European adults follow football, rising to more than 70% among UK men aged 25-54 - a key car-owning demographic. Pitch-side LED advertising, kit sponsorships, and tournament broadcast rights put tyre brands in front of these consumers week after week.

But does the spend translate into measurable brand equity? Brand Finance's position has long been that sponsorship is only valuable insofar as it shifts the metrics that ultimately drive revenue. Consideration is one such metric; our valuation models suggest that each one-point gain in consideration correlates with roughly a 0.6% rise in market share. However, the metric most closely linked to revenue is usage itself: whether consumers have actually purchased the brand in the past 12 months. Awareness, familiarity, consideration, and preference are all important, as they reflect different stages of the customer journey.

Ultimately, though, usage is the strongest indicator of whether sponsorship has successfully converted attention into customers. To assess how today’s tyre sponsors are performing, we segmented our November 2025 Global Brand Equity Monitor data into football fans and non-fans, measuring uplift across key brand equity metrics for seven tyre brands with active football partnerships in Europe or the UK. We report both the pan-European average and the UK results, where football engagement is highest.

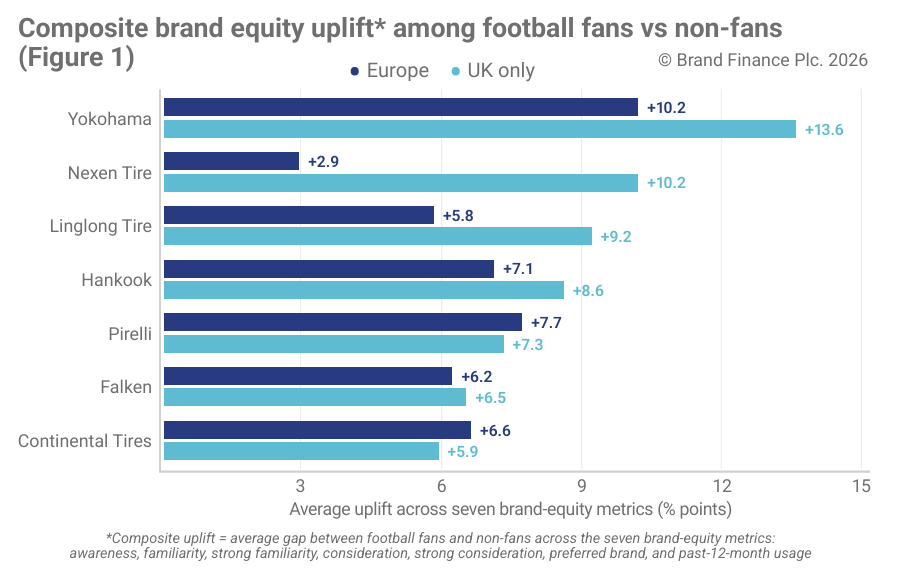

The verdict: Seven brands, two telling pictures

Yokohama tops both panels (See Figures 1 & 2) – a remarkable result given that Linglong Tire replaced it as Chelsea’s Global Tyre Partner in 2024. The findings highlight just how enduring sponsorship equity can be.

Nearly two years after the partnership ended, UK football fans are still 22.8 percentage points more likely to be aware of Yokohama than non-fans, and 22.0 points more likely to be familiar with the brand.

Manchester City sleeve sponsor Nexen Tire and Chelsea’s current tyre partner Linglong rank second and third respectively in the UK panel, with Hankook close behind. The transition from Yokohama to Linglong is therefore far from a clean handover.

Instead, it represents a period of co-existence at the top of the rankings: Yokohama continues to benefit from the legacy of its long-standing Chelsea partnership, while Linglong – alongside Manchester City partner Nexen – is steadily building sponsorship equity of its own.

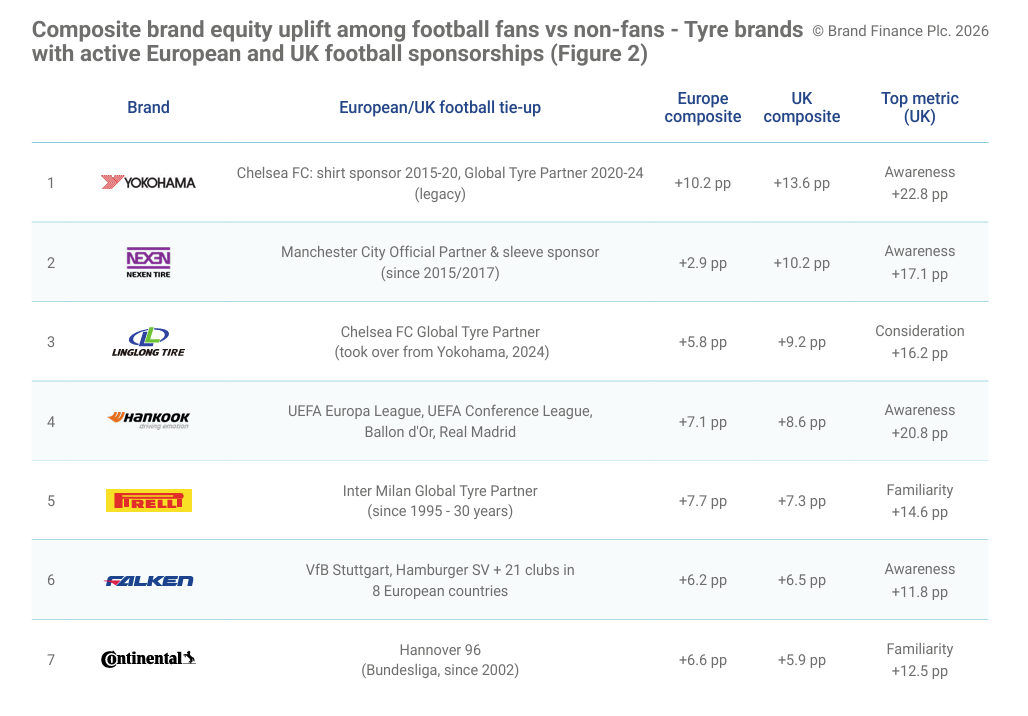

Asia buys, Europe watches

A striking feature of the line-up is that five of the seven tyre sponsors are headquartered in Asia. Yokohama and Falken (Japan), Linglong (China), and Nexen and Hankook (South Korea) are all leveraging European and UK football to build awareness

and consideration in markets where they are still establishing themselves against long-standing incumbents such as Pirelli and Continental.

In many ways, football has become a route to market for ambitious Asian tyre brands seeking to scale their presence in Europe.

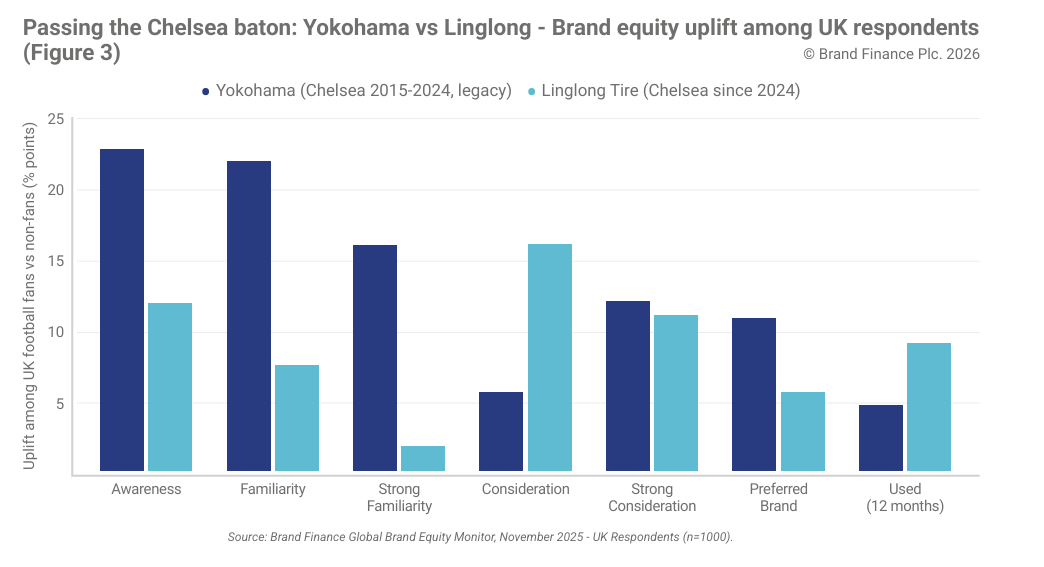

Awareness: The legacy halo

Yokohama’s dominance reflects nearly a decade as Chelsea’s shirt sponsor and global tyre partner between 2015 and 2024. Sponsorship equity, however, does not disappear when a deal ends. Even a year after Linglong took over the Chelsea partnership, Yokohama’s uplift (Figure 3) among UK football fans remains almost twice as high on both awareness (+22.8 vs +12.0 percentage points) and familiarity (+22.0 vs +7.7 points).

Hankook, UEFA Europa League partner since 2012 and now a sponsor of the Ballon d’Or, records the second-highest awareness uplift in the UK at +20.8 points. Nexen, Manchester City’s sleeve sponsor since 2017, follows at +18.6 points – a notable result for a brand that had limited visibility in Europe just a decade ago.

Meanwhile, Falken’s strategy of pursuing breadth rather than depth, with partnerships spanning 21 clubs across eight countries, delivers a respectable +11.8-point awareness uplift at a fraction of the cost of a top-tier kit deal.

Familiarity: The heritage premium

Awareness is necessary but rarely sufficient.

Familiarity - the sense that a buyer actually knows a brand - is where long-running partnerships earn their keep.

Pirelli leads on Strong Familiarity in the UK (+14.1 pp), the dividend on a 30-year relationship with Inter Milan that ranks among the longest brand club marriages in world football. Yokohama (+16.1 pp UK) and Continental (+10.3 pp UK) demonstrate the value of long-term investment, with more than a decade of visibility in Europe’s top football competitions translating into significantly stronger consumer familiarity.

Linglong, now in its second season as Chelsea’s tyre partner, records a modest +2.0-point familiarity uplift, while Nexen posts +4.1 points. The results serve as a reminder that deep consumer associations are built over years, not seasons.

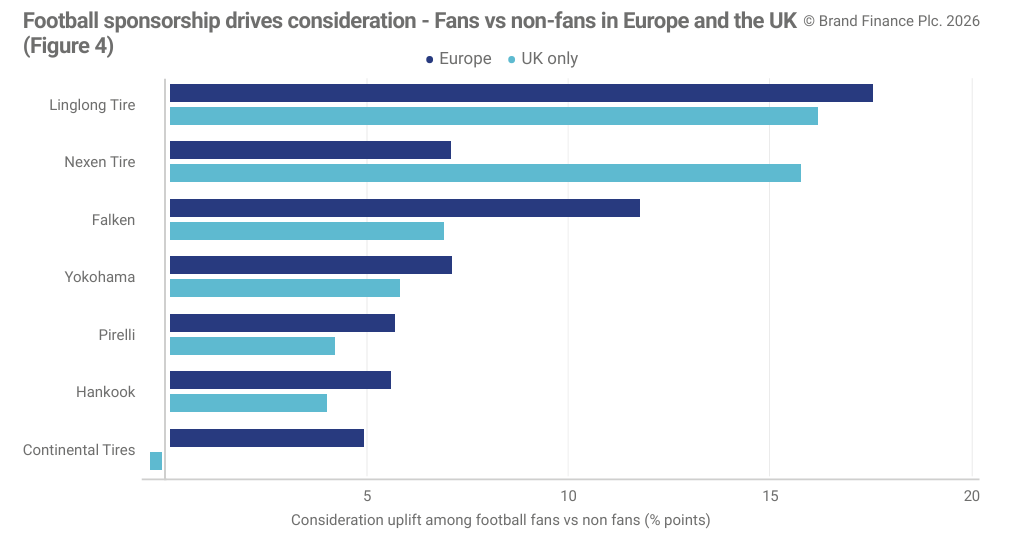

Consideration: Where the funnel turns

Consideration is the metric most directly tied to the short-term sales pipeline, and here the rankings reshuffle (Figure 4). Linglong posts the largest consideration uplift in the dataset: UK football fans are 16.2 percentage points more likely to consider the brand than non-fans, rising to 17.6 points across 20 consumers from “I might consider” to “I would definitely consider.” It is at this stage of the funnel that the value of long-term brand heritage becomes most apparent. Usage: Where sponsorship becomes revenue Brand equity ultimately matters because Europe overall. Nexen follows closely behind in the UK at +15.8 points, with Falken (+6.9 points) and Yokohama (+5.8 points) some way back.

The pattern is instructive: challenger brands may trail established players on awareness and familiarity, but they can still translate sponsorship exposure into consideration when partnerships are highly visible and consistently activated.

Nexen is also the leader on Strong Consideration (Top-2 Box) in the UK, with a +17.1 pp uplift - the largest in the entire dataset and a striking result for a brand that did not feature on UK retailer shelves a decade ago. Pirelli, meanwhile, demonstrates the power of an established brand. Despite already enjoying near universal consideration among European football fans (87.5%), it gains a further +9.2-point uplift on Strong Consideration in the UK.

Usage: Where sponsorship becomes revenue

Brand equity ultimately matters because it converts into sales. Usage – having purchased or fitted the brand in the past 12 months – is the closest survey proxy we have for revenue, and the UK results are particularly striking. Linglong Tire posts a +9.2-point usage uplift among UK football fans, the highest in the dataset and a strong early indication that the Chelsea partnership is driving tangible commercial outcomes, not just awareness

Yokohama (+4.9 pp UK), Falken (+3.9 pp) and Pirelli (+3.6 pp) complete a strong-performing top four. In each case, football fans are not only more aware of the brand, but also more likely to have purchased it.

Continental sits just above zero (+0.8 pp), while Hankook is marginally negative. Usage is also the metric most influenced by category demographics, as football fans tend to skew younger and more urban, with proportionally fewer tyres to purchase each year.

The preferred-brand paradox: Nexen Tire

Nexen Tire provides the most interesting outlier in the study. UK football fans are 9.9 percentage points more likely than non-fans to name Nexen as their preferred tyre brand (11.0% vs 1.1%) - the highest preference uplift in the study after Yokohama.

This is compelling evidence that its long-running Manchester City sleeve partnership is delivering meaningful brand-building returns. However, on past-12-month usage, Nexen records a 7.1 percentage point deficit among football fans. The same fans who say they prefer Nexen are not (yet) buying it. This reflects what Brand Finance has long described as the lead-lag effect of sponsorship returns: brand equity tends to build first, while sales conversion follows over a much longer timeframe.

For Nexen, the foundations for future revenue growth appear firmly in place. The challenge now is translating preference into purchase, and the renewal of the Manchester City partnership for a third term suggests both parties believe that conversion will come with time.

Lessons for sponsors

Three takeaways stand out. Firstly, sponsorship equity is sticky: Yokohama's top-of-table position a year after handing the Chelsea baton to Linglong shows that the dividends of a well-chosen, long-running partnership decay slowly.

Secondly, the right Premier League partnership can fast-track a challenger brand from obscurity to a measurable usage lift in a single season - Linglong's +9.2 pp UK usage uplift is the single most important data point in this study, because it links sponsorship directly to revenue.

Thirdly, brands with established heritage (Pirelli, Continental) deliver the most balanced uplift across the funnel, while newer entrants to the category (Linglong, Nexen) generate disproportionate gains at one or two stages of the customer journey - awareness, consideration and preference - where their partnerships are having the greatest impact, with usage to follow.

For tyre brands weighing their next investment, the question is not whether football sponsorship works - the data clearly shows that it does - but whether the chosen partnership can drive usage, not just awareness. Done well, and maintained over time, the right sponsorship can elevate every step of the customer journey at once.

Methodology

Data drawn from Brand Finance's Global Brand Equity Monitor, November 2025 wave. Europe filter covers respondents in the UK, Spain, Italy, Germany, Austria, France and Switzerland (n = 750 to 4,751 per brand). UK-only panel: n = 1,000 (range 215 to 714 per brand for QN4 and QN5). Football fans are respondents who said they follow football (soccer) in-person, on TV or online (Q15). Brand metrics from Q1 (awareness/ familiarity), QN5 (consideration/preference) and QN4 (usage). Uplifts shown in percentage points (fans minus non-fans). Brands shown are restricted to those with verified active European or UK football team or tournament partnerships in the 2025/26 season; Yokohama is included on a backwards-looking basis given its 2015 2024 Chelsea FC relationship. Kumho Tire was excluded because the UK panel did not include the brand.