Brand Finance’s Cosmetics 50 2026 ranking reveals an industry-wide slowdown, reflected in a 6% total brand value decline

LONDON, 5 May 2026 – French cosmetics brands continue to dominate the ranking this year, accounting for 47% (USD68.5 billion) of the sector’s total brand value. The US follows in second place, with a 35% share (USD50.4 billion) and Germany in third, with a 6% share (USD10.1 billion). According to the Cosmetics 50 2026 ranking by Brand Finance, the world's leading brand valuation consultancy, the cosmetics sector faces industry-wide headwinds, reflected in a 6% decline in collective brand value to USD149.8 billion this year.

Over the past year, geopolitical and economic uncertainties have significantly impacted major economies worldwide, causing a slowdown in the cosmetics industry as growth shifts from price-led to innovation-led. Consumer spending within the sector has also changed, with customers cutting back on non-essential purchases while increasingly demanding quality and performance rather than paying premium prices without clear proof of effectiveness. Additionally, global climate volatility continues to push demand for climate-adaptive formulations and innovations that focus on skin longevity, barrier protection, and weather-responsive products.

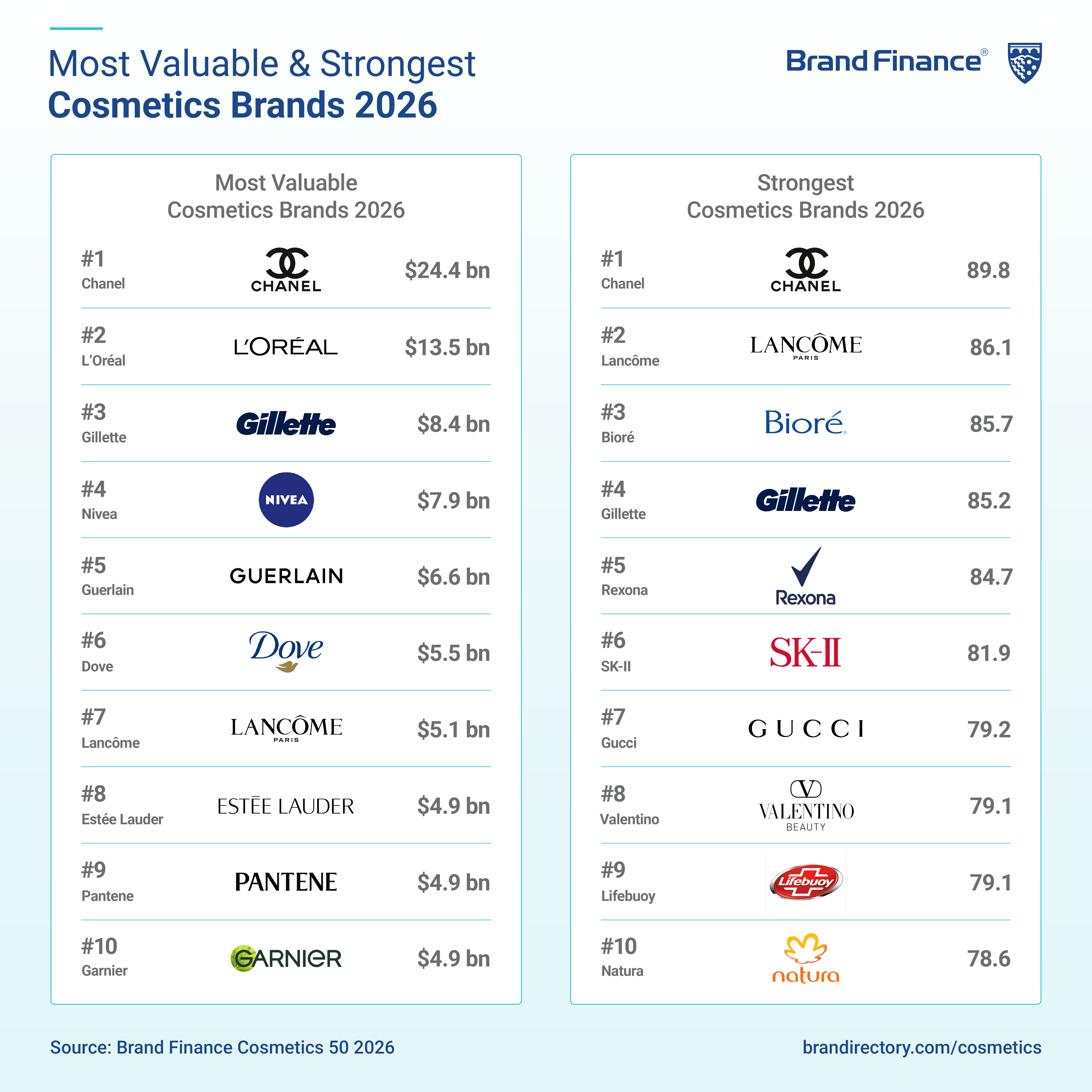

Despite sector-wide headwinds and a brand value dip, Chanel (brand value down 11% to USD24.4 billion) achieves a double win by retaining its position as the most valuable brand and rising two spots to become the strongest brand in the ranking this year. Chanel’s brand value decline is a result of revenue forecast drops in China and the US, the sector’s largest markets, due to challenging macroeconomic conditions such as a housing crisis and rising unemployment rates, which caused consumers to be more selective of their spending and shift toward local and economical brands. However, this is likely to be a short-term setback, as Chanel continues to drive long-term value creation through its iconic brand, and this year saw an increase in brand strength due to improved reputation, engagement, consideration, and price acceptance, receiving a Brand Strength Index (BSI) score of 89.8/100 and an AAA+ brand strength rating, a notable increase from its 87.7/100 BSI score and AAA brand strength rating in 2025.

L'Oréal (brand value down 13% to USD13.5 billion) ranks as the second most valuable cosmetics brand despite a decline in brand value caused by the same economic headwinds that impacted more than 60% of the featured brands in the ranking. The brand retains its position due to its diversified portfolio, which helped mitigate financial risks as its financial performance reports modest revenue growth that falls short of expectations. L'Oréal’s dermatological beauty segment grew less than 1%, reflecting an industry-wide trend where growth is driven by price increases instead of expansion in sales volumes.

Gillette maintains its position as the third most valuable brand in the ranking despite an 8% brand value decline to USD8.4 billion this year, caused by shifts in facial care trends for men. In 2025, the shaving product segment recorded an industry-wide value loss as traditional razor routines were replaced by beard maintenance and styling solutions across the US, Europe, and India. However, this year also marks the end of Gillette’s 2-year reign as the strongest global cosmetics brand, a reflection of growing competitive pressure from new entrants such as Dollar Shave Club and Harry’s that have scaled up over the past decade.

Bulgari sees a notable 41% brand value increase to USD1 billion, making it the fastest growing cosmetics brand this year. Although its parent company, LVMH, recorded a dip in revenue, the Italian luxury brand experienced a noteworthy year, generating record sales of multi-million-dollar pieces from its ‘Polychroma’ collection, which combines the artistry of high jewellery with haute couture fragrances. The brand has also expanded its market reach by establishing new flagship stores in Milan, Los Angeles, Miami, Tokyo, and Riyadh. Bulgari’s performance was also supported by several campaigns, including a Serpenti-focused programme featuring the Serpenti Infinito exhibition in Shanghai to commemorate the Year of the Snake, and the ‘Eternally Reborn’ campaign, centred on the continuous reinvention of Bulgari’s identity, designs, and craftsmanship.

Lancôme (brand value down 17% to USD5.1 billion) maintains its position as the second strongest brand in the sector despite declines across metrics such as familiarity, credibility, appeal, and price acceptance. The luxury beauty brand receives a BSI score of 86.1/100, a slight dip from last year’s 88.4/100, while maintaining its AAA brand strength rating. This decline in brand strength can be attributed to the gradual alienation of customers due to years of aggressive price increases across the luxury sector, leading consumers to choose more economical brands.

Bioré (brand value up 15% to USD976 million) stands out for its 29-spot leap to become the third strongest brand in the ranking this year, receiving a BSI score of 85.7/100 and an AAA brand strength rating. This year, the brand launched Bioré UV Aqua Rich Watery Hold Cream sunscreen, which was developed based on consumer feedback that the use of sunscreen has become a habit, with 48% of the respondents citing that they now apply sunscreen all year round. The skincare brand also partnered with Stray Kids, one of the most celebrated K-pop groups, for a global campaign encouraging people to enjoy activities under the sun.

Annie Brown, Managing Director UK, Brand Finance, commented:

“The global cosmetics sector is entering a period of recalibration, where scale alone is no longer enough to sustain growth. While iconic brands such as Chanel and L’Oréal continue to lead in value, shifting consumer expectations and economic pressures are redefining success. Brands that can maintain desirability, respond to climate realities, and rebuild trust around pricing will be best positioned to win. Ultimately, resilience in today’s market is increasingly shaped by relevance, agility, and meaningful consumer engagement.”

Other notable brands featured in the Brand Finance Cosmetics 50 2026 ranking include:

Sustainability

The 2026 Sustainability Perceptions Index reveals which brands are perceived to have the strongest commitment to sustainability globally, the changing role of sustainability in driving demand, and the significant value tied to sustainability for the world’s biggest brands.

Sustainability is a key driver of consumer choice and reputation in the cosmetics sector, driving 3% of consideration. Brand Finance research reveals that The Body Shop, Garnier, and NARS lead sustainability perceptions for the Environmental, Social, and Governance (ESG) pillars, respectively.

The Body Shop’s refill programmes remain a core sustainability initiative, operating across hundreds of stores globally to cut single-use plastic and lower the cost per use for customers.

Garnier’s partnership with Plastics for Change evolved into a structured social‑protection model, that provides informal waste collector communities with access to fair pay, insurance access, identity documentation, and safer working conditions.

NARS’s parent company, Shiseido, established its Sustainability Strategy Acceleration Office, aimed at integrating sustainability-related functions, driving the group’s strategic initiatives, and enhancing its ability to address social and environmental issues.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.