New Brand Finance data shows Chinese brands account for five of the world’s top 10 real estate brands despite sector challenges

BEIJING, 30 June 2026 – China remains the world’s largest real estate brand market, although the combined value of Chinese real estate brands in the Brand Finance Real Estate 25 2026 ranking has fallen 29% to USD27.6 billion as the prolonged property downturn continues to weigh on developer performance, investor sentiment, and consumer confidence.

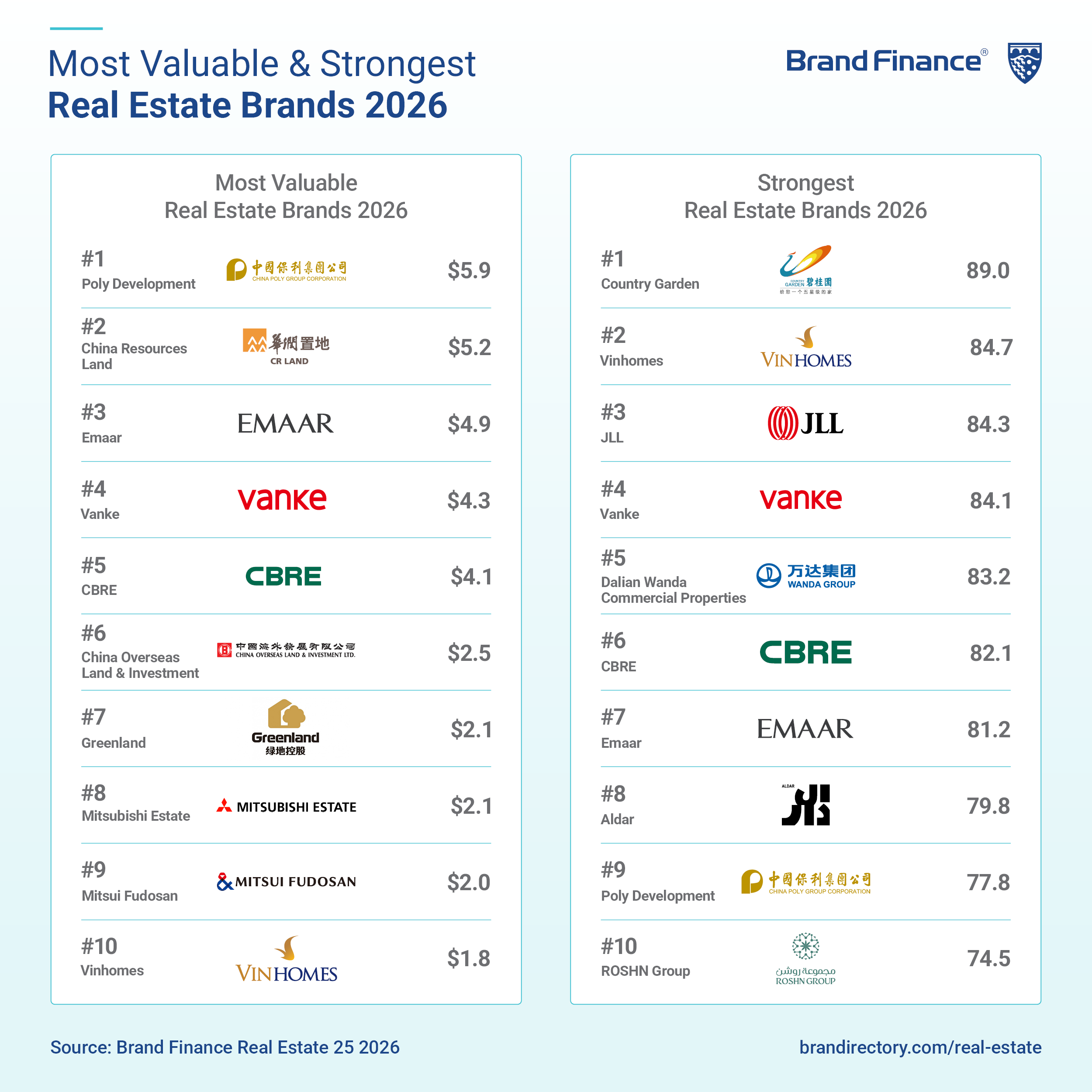

According to the latest Real Estate 25 2026 report, Chinese brands continue to dominate the global real estate landscape, accounting for five of the world’s 10 most valuable real estate brands. However, weaker home sales, declining property prices, and ongoing liquidity challenges in its local market have significantly impacted brand values across the sector.

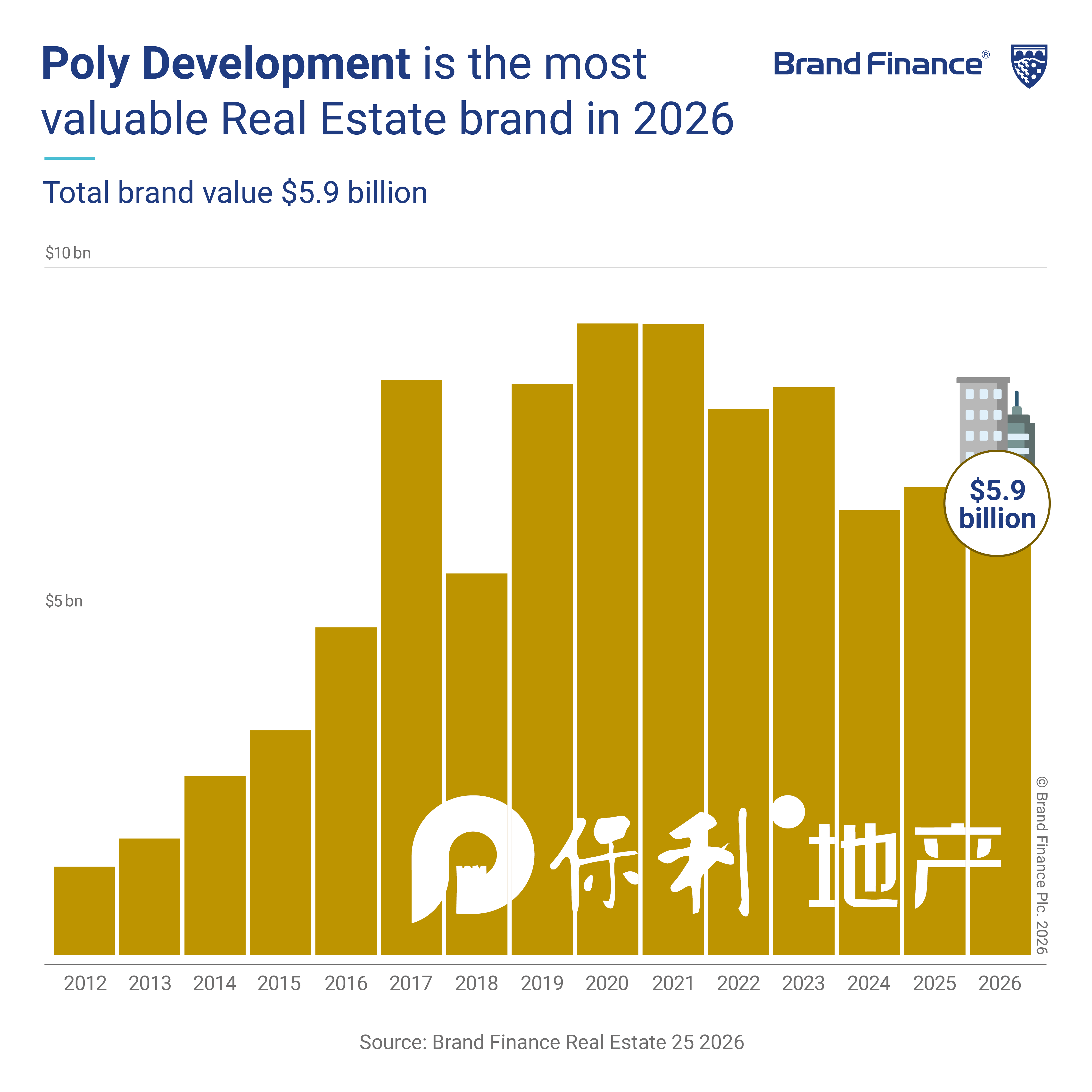

Despite these pressures, Poly Development (brand value down 12% to USD5.9 billion) emerges as the most valuable real estate brand globally for the first time. While the company continues to face the same market headwinds affecting the wider industry, its state-backed positioning, comparatively resilient market performance, and stronger perceptions of stability have supported its rise to the top of the global ranking.

China Resources Land (brand value down 28% to USD5.1 billion) retains second place globally. Although softer contract sales and weaker development sentiment weighed brand performance, stable recurring income from its commercial property portfolio helped mitigate some of the pressure.

Meanwhile, Vanke (brand value down 43% to USD4.2 billion) recorded one of the steepest declines among the world’s leading real estate brands as weaker contracted sales, lower profitability, and liquidity concerns continued to affect market confidence.

China Overseas Land & Investment (brand value down 2% to USD2.5 billion) proved comparatively resilient, supported by improvements in stakeholder perceptions and stronger confidence in its long-term stability.

Greenland (brand value down 11% to USD2.1 billion) continued to face challenges as declining revenues, debt concerns, and reduced development activity weakened both financial performance and brand perceptions.

Scott Chen, Managing Director China, Brand Finance, commented:

“China remains the world’s largest real estate brand market, but the sector is undergoing a profound structural adjustment. The 2026 results demonstrate that brand strength has become increasingly important during periods of market uncertainty. Developers perceived as financially resilient, operationally stable, and capable of delivering long-term value are proving better positioned to maintain stakeholder confidence. Poly Development’s leadership and the resilience of several state-backed developers illustrate how trust and stability have become critical competitive advantages in China’s evolving real estate market.”

Despite significant financial pressure, Country Garden (brand value down 68% to USD1.3 billion) ranks as the strongest real estate brand globally, with a Brand Strength Index (BSI) score of 89/100 and an AAA brand strength rating. Its strength reflects high legacy awareness in China’s residential market, although perceptions of trust, delivery certainty, and financial stability remain under pressure following debt restructuring challenges.

Brand Finance’s market research data also reveals a widening gap between developers perceived as financially secure and those facing liquidity concerns. State-backed developers have generally strengthened their relative positions, benefiting from stronger perceptions of stability and government support, while privately owned developers continue to face greater scrutiny from investors and homebuyers.

Although market conditions remain challenging, Chinese brands continue to occupy a central position in the global real estate industry. The long-term recovery of the sector is expected to depend on improving homebuyer confidence, stabilising market fundamentals, and rebuilding trust among stakeholders.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.