New data from Brand Finance reveals China’s top 11 mining brands are valued at $17.7 billion, with eight brands registering growth

BEIJING, 24 April 2025 – The combined brand value of China’s 11 leading mining, metals & minerals brands remains stable at USD17.7 billion, accounting for almost a quarter of the ranking’s total value, according to the latest Mining, Metals & Minerals 2025 report by Brand Finance, the world’s leading brand valuation consultancy.

While the world’s mining sector faced a range of challenges, including commodity price volatility, geopolitical tensions, and the global energy transition to renewable energy technologies, Chinese mining brands remain highly competitive with eight brands registering an uptick in brand value.

Jiangxi Copper (brand value down 12% to USD3.7 billion) ranks fourth globally and remains as China’s most valuable mining brand for the third consecutive year since its debut in 2023.

China’s reduced consumption and the oversupply of steel led to a slight decline in BAOWU’s brand value (down 5% to USD2.5 billion). Even so, the brand managed to secure its place as China’s strongest mining brand - having previously ranked fourth strongest in 2024 - with a Brand Strength Index (BSI) score of 62.4/100 and a brand strength rating of A+.

China Hongqiao Group (brand value up 27% to USD865 million) is China’s fastest-growing mining brand for 2025. The brand’s strong performance is underpinned by a modest increase in sales volume and a notable rise in gross profit margin for primary aluminium products driven by improved selling prices and effective cost management. Its USD1.8 billion investment in the Simandou project signals a strategic move to secure upstream resources and enhance supply chain resilience, reinforcing its growth trajectory and brand value.

Scott Chen, Managing Director, Brand Finance China, commented:

“Despite headwinds from global market volatility and the ongoing energy transition, China’s mining brands have demonstrated remarkable resilience and adaptability. With eight of the 11 Chinese mining brands recording brand value growth this year, including standout performances from Jiangxi Copper, BAOWU, and China Hongqiao Group, it’s clear that strategic investments, improved margins, and supply chain strength are helping to drive brand value within China’s mining industry.”

Meanwhile, other notable Chinese mining brands featured in the global rankings are:

Brand Finance has identified the top-performing brands across six key industrial categories: steel production, aluminium production, coal, copper mining, copper processing, and iron. Chinese brands are leading in three of these six categories and consistently rank among the top five across all, showcasing the nation's growing global influence in the extractive and metallurgical sectors.

Sustainability

Brand Finance also assesses the brands consumers consider most committed to sustainability. The 2025 Sustainability Perceptions Index will be released later this year, revealing which brands are perceived to have the strongest commitment to sustainability globally, the changing role of sustainability in driving demand, and the large amounts of value at risk, being missed, and being secured by the world’s biggest brands.

Kobelco is the top-ranked mining brand in the rankings for its environmental sustainability perceptions. Meanwhile, Citic Pacific Mining is highly regarded for its social sustainability efforts, and Acerinox leads in governance sustainability.

Global Insights

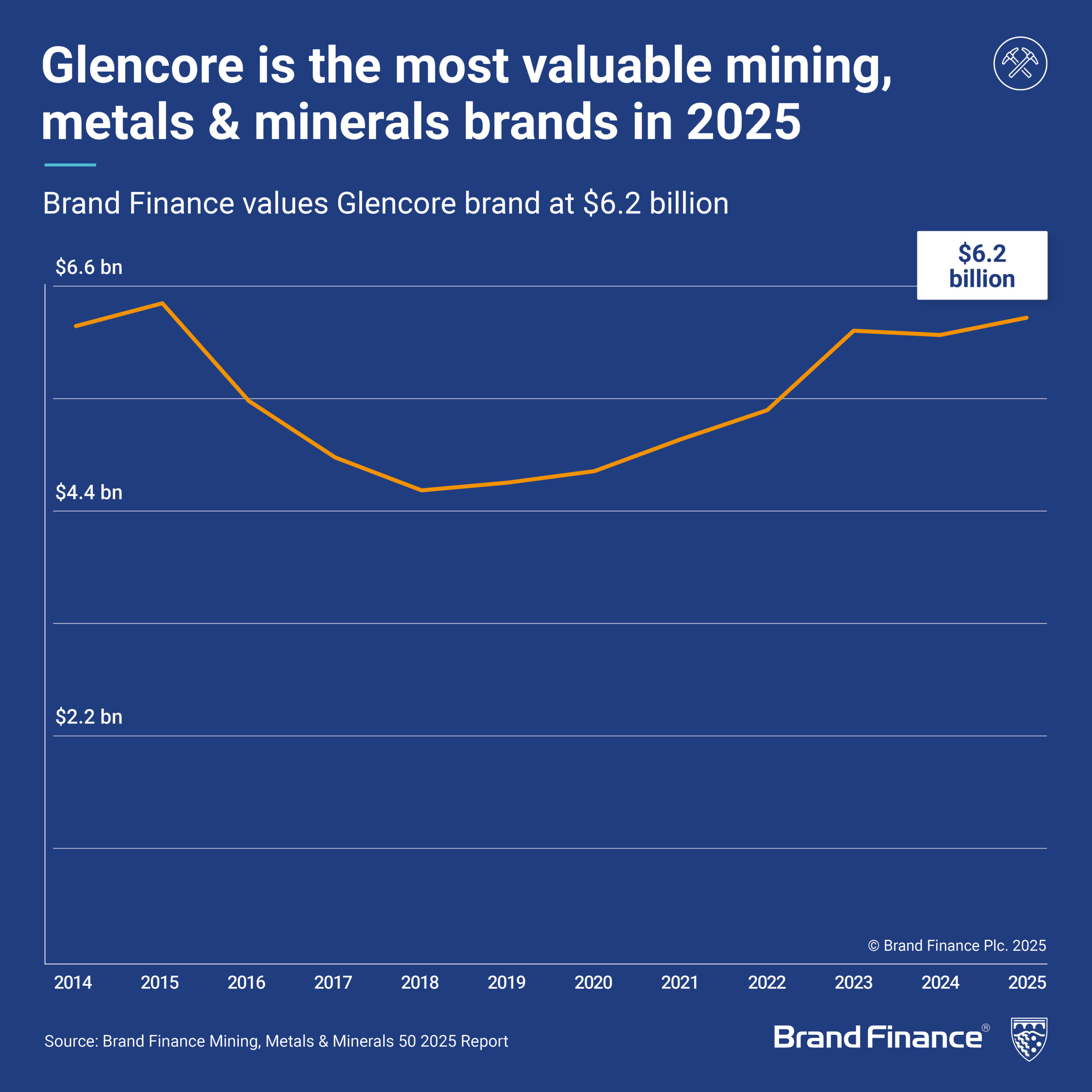

Glencore (brand value up 4% to USD6.2 billion) has reclaimed its position as the world’s most valuable mining brand, surpassing BHP (brand value down 17% to USD5.1 billion).

Posco Steel (brand value up 16% to USD2.7 billion) is the world’s second strongest mining, metals, and minerals brand with a BSI score of 78.5/100 and an AA+ brand strength rating.

Steel Dynamics (brand value up 36% to USD894 million) is the fastest-growing brand in this sector for 2025. The brand’s growth is fuelled by strong financial performance and strategic market positioning.

Specialist audience research methodology

This is the second year of primary multi-stakeholder specialist audience research in Mining, Metals & Minerals sector. The analysis captures insights from a global network of senior decision-makers and business transformation leaders, offering actionable findings to help brands grow both their brand equity and commercial impact.

The study covers 15 major brands, including Ma’aden, Barrick Gold, BHP, ArcelorMittal, Phosagro, Newmont, Vale, Anglo American, Rio Tinto, Mosaic, Freeport-McMoRan, Glencore, OCP, Emirates Global Aluminium (EGA), and Alcoa.

The research evaluates brand performance through a wide range of Brand and Reputation metrics, including brand funnel stages (knowledge, consideration, usage, and recommendation), brand image and personality (reputation, strategy, and quality), as well as 18 functional image drivers such as value, innovation, culture, and emotional connection.

Geographically, the study covered a 350 specialist sample from five key regions: Asia (32% respondents), the Americas (29%), Europe (25%), Africa (11%), and Australia (3%).

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.