New Brand Finance data shows the Netherlands’ top 50 brands are valued at €147.6 billion in 2026, up 13% year-on-year

LONDON, 17 June 2026 – The Netherland’s top 50 brands have grown by 13% to reach a combined value of EUR147.6 billion in 2026, according to the Netherlands 50 2026 ranking by Brand Finance, the world’s leading brand valuation consultancy.

The Netherlands entered 2026 on relatively solid economic footing, with a GDP growth of 1.9% in 2025 driven by exports and domestic demand, though momentum is expected to moderate amid weaker investment, global uncertainty, and structural constraints including energy grid congestion and nitrogen regulations, although lower interest rates and stronger economic activity in Germany are expected to provide some support.

Oil & gas remains the Netherlands’ most valuable sector, anchored by Shell, following a volatile year driven by energy price swings and LNG-led recovery. Banking is the standout growth sector, rising 18% to EUR26.6 billion as Dutch banks accelerate green finance, digital transformation, and ESG-linked lending, with ING and ABN AMRO central to major sustainable infrastructure financing. Together, these sectors highlight the continued strength of scale-driven industries, even as energy transition pressures and shifting capital priorities reshape long-term trajectories.

Commercial services stand as the most polarised sector, with Wolters Kluwer’s strong operational performance offset by a sharp brand value drop (brand value down 26% to EUR2.2 billion), while Randstad (brand value 19% to EUR2.2 billion)continues to decline amid structural labour market shifts and weakening demand for traditional staffing. Retail & e-commerce records the steepest fall, down 19%, as online price competition and evolving consumer behaviour erode non-grocery retail, while supermarkets remain resilient, reinforcing a clear essential-versus-discretionary divide. In contrast, Beers vs Soft Drinks highlights divergent growth models, where beer brands like Heineken build value through premiumisation and global equity, while soft drinks’ growth is increasingly driven by portfolio expansion and acquisitions rather than core brand strength.

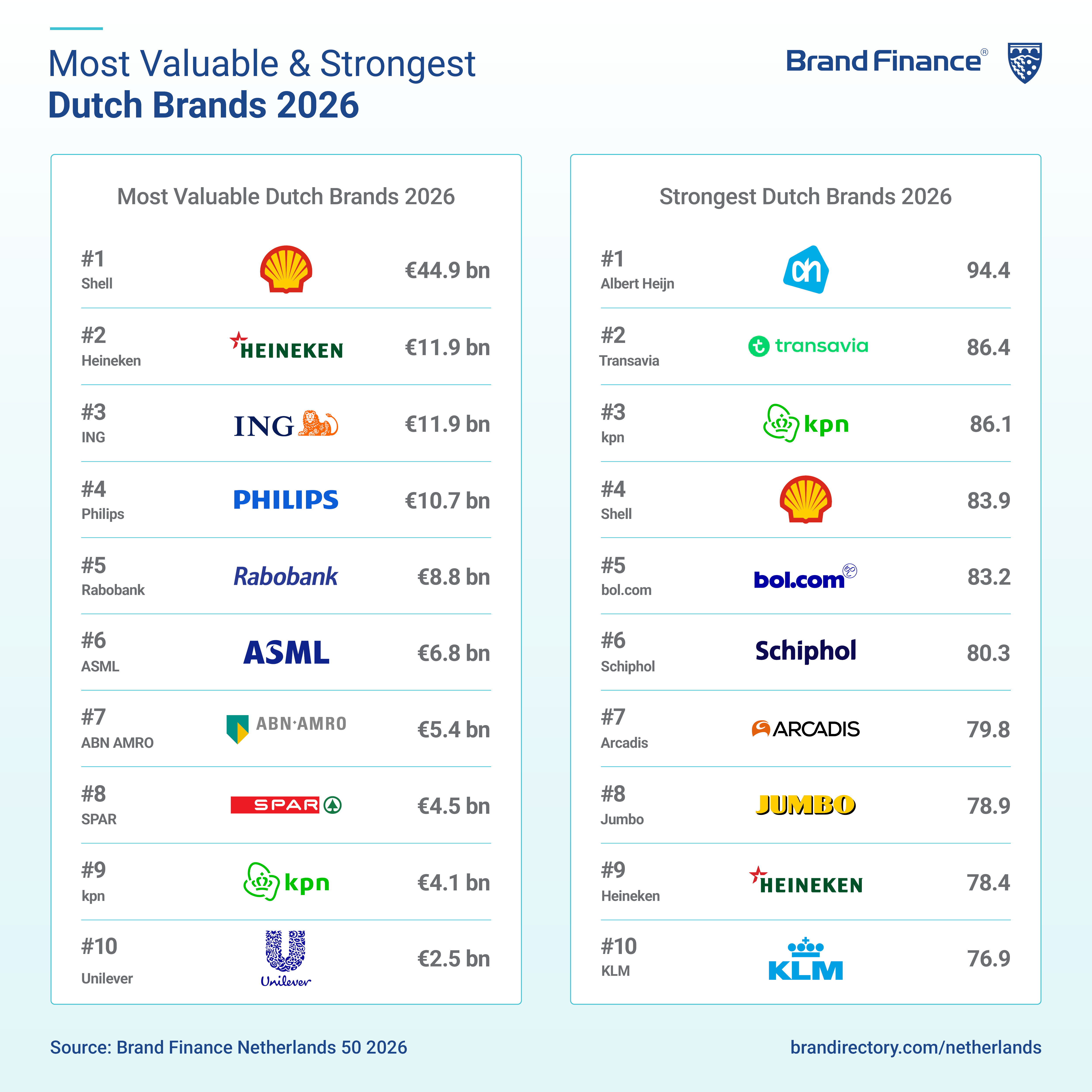

Shell (brand value up 10% to EUR44.9 billion) retains its position as the Netherlands’ most valuable brand for the 16th consecutive year, supported by improved revenue forecasts. Growth is driven by volume recovery and a strategic shift towards higher-return segments, rather than solely higher energy prices. The company continues to prioritise LNG, upstream production, mobility retail and lubricants, strengthening revenue stability through higher LNG sales volumes, improved marketing margins, and disciplined portfolio optimisation that supports profitability amid ongoing commodity volatility.

Heineken (brand value up 3% to EUR11.9 billion) keeps its second rank, remaining stable year-on-year despite a softer market and slight downward pressure on revenue forecasts, supported by continued strength in its premium and alcohol-free portfolio. The brand is accelerating innovation in low- and no-alcohol offerings, including experimental launches such as Heineken 0.0 Ultimate and Heineken Fusion, as it seeks to future-proof growth beyond traditional beer consumption. This is reinforced by strong brand-building activity, with sports-led marketing, particularly around UEFA Women’s Champions League activations, strengthening Heineken’s positioning in lifestyle and fan engagement spaces.

ING (brand value up 22% to EUR11.9 billion) remains third, recording strong growth supported by more favourable Weighted Average Cost of Capital (WACC) and long-term growth assumptions, alongside sustained operational momentum. Performance is driven by net fee and commission income, which grew around 4% year-on-year and delivered a third consecutive record quarter in 2025. Additionally, the bank stands out for its ESG efforts in sustainable finance and grew its mobile customer base to 1.1 million in 2024 to support its digital-first strategy.

Henry Farr, Valuation Director, Brand Finance commented:

“Dutch brands in 2026 reflect an economy defined by resilience in core sectors and growing divergence across the market. Established leaders are maintaining strength by actively reshaping their business models, whether through energy transition strategies, digital transformation, or continued investment in innovation and brand experience. At the same time, the fastest-growing brands highlight how quickly value can be created where demand recovery and operational scaling align, particularly in travel and consumer-facing sectors. However, this growth sits alongside sharper structural pressures in retail and commercial services, where shifting consumer behaviour and labour market dynamics are increasingly driving a clear separation between resilient and vulnerable brand categories.”

Albert Heijn (brand value down 13% to EUR1.2 billion) is the Netherlands’ strongest brand in 2026, with a Brand Strength Index (BSI) score of 94.4/100 and an AAA+ brand strength rating. According to Brand Finance’s market research data, familiarity and consideration remain high, supported by rising engagement driven by the Bonuskaart ecosystem and AH app, which reaches over 10 million users and supports most transactions. The brand strengthens its position through hybrid dairy innovation, AI-led food waste reduction of over 2 million kg, and sustainability leadership including methane emissions disclosure, while improved perceived value also supports stronger price acceptance.

Transavia (brand value up 49% to EUR439 million) ranks second, with a BSI score of 86.4/100 and an AAA brand strength rating. The brand demonstrates strong familiarity and operational performance, supported by sustained demand in the low-cost leisure travel segment. Transavia is also the fastest growing brand in this year’s rankings, with its growth driven by higher passenger volumes and network expansion, carrying over 12 million passengers in the first half of 2025, up 11% year-on-year, alongside a 12% increase in capacity. Despite this expansion, Transavia continues to operate at high seat occupancy levels, while improved pricing and yield performance supports further revenue growth.KPN (brand value up 5% to EUR4.1 billion) ranks third with a BSI score of 86.1/100 and an AAA brand strength rating. The brand sees a slight decline in its BSI year-on-year (86.1/100 in 2025), with weaker performance in reputation and consideration metrics. This is partly influenced by a major mobile network outage in 2025, which generated more than 26,000 reports and caused widespread disruption to mobile connectivity, including difficulties accessing emergency services. Despite this, KPN maintains a strong overall brand strength position, supported by its established market leadership and critical infrastructure role in the Netherlands.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.