29 February 2024, LONDON – Sweden has dropped 1 rank to 12th in the 2024 Global Soft Power Index, according to a new report from Brand Finance, the world's leading brand valuation consultancy. This follows a decline in global perceptions of Sweden’s Reputation (down 2 to 8th) and Familiarity (down 2 to 23rd), despite an overall increase in soft power score, up 3.9 points.

However, Sweden has improved its ranking for Business & Trade, up 1 to 9th. At a time of global uncertainty and instability, economic credentials are increasingly important contributors to a nation’s soft power. Perceptions of Sweden’s ‘future growth potential’ improved dramatically, up 37 to 37th, contributing to its improved Influence on the global stage (up 2 ranks to 22nd).

Further, Sweden continues to perform particularly well on sustainability metrics, ranked 3rd in the world for both ‘sustainable cities and transport’ and ‘acts to protect the environment’. However, this year, Norway overtakes Sweden for the pillar Sustainable Future. Sweden now ranks 4th overall, behind Norway (3rd), Germany (2nd) and Japan (1st).

Anna Brolin, Managing Director of Brand Finance Nordics, commented:

“Overall, Sweden’s performance in the Global Soft Power Index has remained robust, and continues to perform well across several pillars, including Business & Trade, Education & Science, and Sustainable Future. Once more, Sweden leads among its Nordic counterparts, and performs well above those of a similar size. This underscores the significance of Sweden’s deliberate and forward-thinking approach and its role in cultivating soft power”.

On the other hand, Sweden has declined for International Relations, down 2 ranks, falling out of the top 10 to 12th. Global perceptions of Sweden’s historic neutrality have shifted since the nation applied to join NATO in 2023, becoming more closely aligned with Western interests and military alliances.

This year, the Global Soft Power Index identified growing concerns around disinformation as a key trend. As individuals become more sceptical about the information they consume through social media and global news, Media & Communications is increasingly important to a nation’s soft power. All Nordic countries fell for the pillar in this year’s Index, with Sweden falling 8 ranks to 16th. Sweden’s rank declined across three out of four attributes: ‘affairs I follow closely’, ‘influential media’, and ‘trustworthy media’. Intensified by language barriers and a comparatively smaller market size, Sweden, along with other Nordic nations, now faces challenges in dispelling scepticism and extending its influence and reach on the global stage.

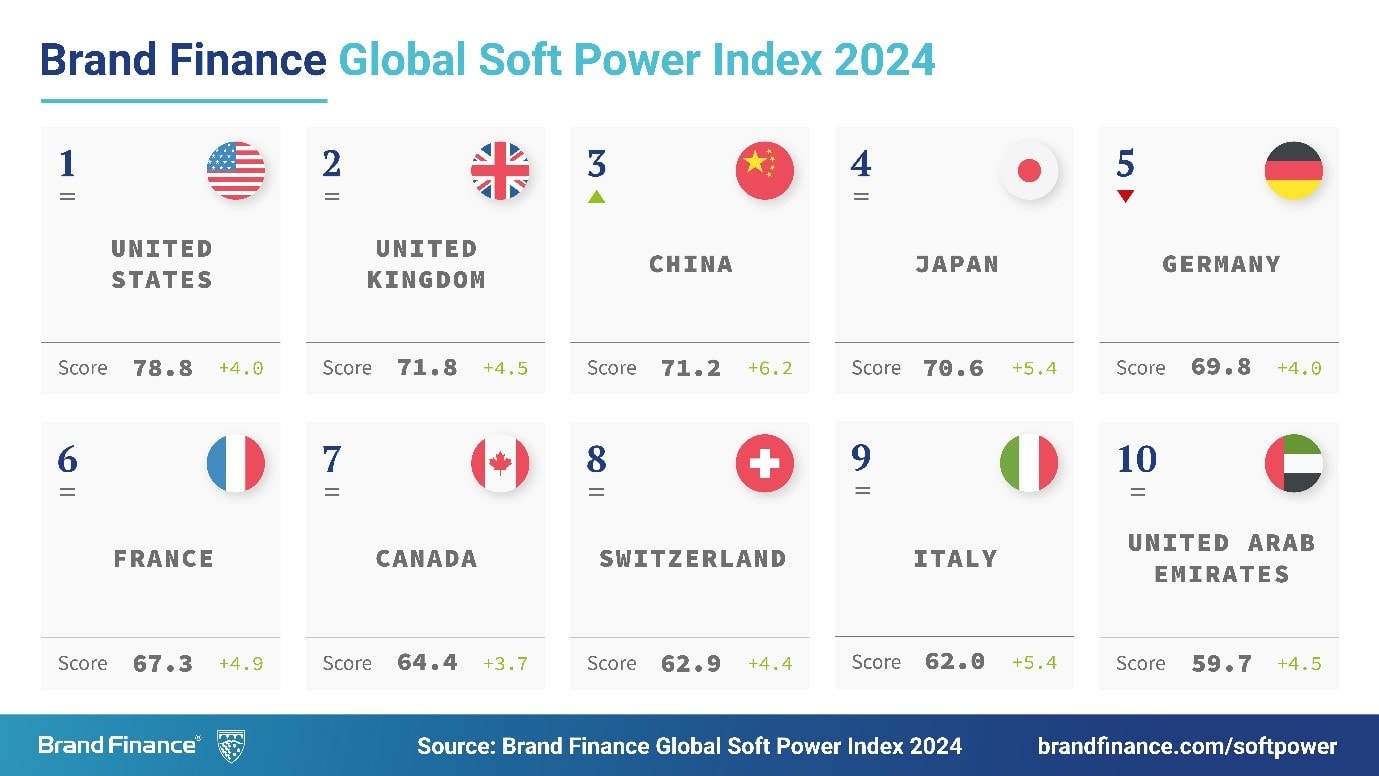

Elsewhere, the United States and the United Kingdom are the most influential soft power nations in the world, China is ranked 3rd, surpassing Japan and Germany.

Brand Finance publishes the Global Soft Power Index based on a survey of more than 170,000 respondents from over 100 countries to gather data on global perceptions of all 193 member states of the United Nations. Thanks to the scope of the survey, the Index is the world’s most comprehensive study on perceptions of nation brands, providing an in-depth analysis of the evolving status of soft power as nations navigate significant global changes and challenges.

Soft power is defined as a nation’s ability to influence the preferences and behaviours of various actors in the international arena (states, corporations, communities, publics, etc.) through attraction and persuasion rather than coercion. Each nation is scored across 55 different metrics to arrive at an overall score out of 100 and ranked in order from 1st to 193rd.

Key Findings of the Global Soft Power Index 2024:

The report has found that – at a time of global uncertainty and instability – economic credentials are increasingly important contributors to a nation’s soft power. Nation brand attributes such as 'strong and stable economy' and 'products and brands the world loves' emerge as key drivers of influence and reputation on the global stage. This trend explains the continued dominance of the world’s largest economies like the USA and China as well as smaller developed economies like Switzerland and the United Arab Emirates at the top of the ranking. Dominant nation brands are recording faster soft power growth (average +3.1 points in the top 50) than the rest of the ranking (average -1.3 for those ranked 51-193).

David Haigh, Chairman & CEO of Brand Finance commented:

“The Global Soft Power Index 2024 underscores the complex interplay between global events and economic shifts in shaping soft power. As nations navigate these dynamics, the importance of a strategic approach to nation branding, supported by perceptions research and financial analysis, becomes increasingly evident.”

The United States leads the rankings with an all-time highest Global Soft Power Index Score of 78.8, an increase from 74.8 in 2023, and earning the top spot for Familiarity and Influence, among other key metrics. However, internal security challenges around gun violence and police brutality as well as involvement in international conflicts seem to be undermining some of its nation brand perceptions, as evidenced by continued rank declines on ‘great place to visit’, ‘good relations with other countries’, ‘safe and secure’, and ‘friendly’ where the USA has dropped a further 9 places to 112th.

The United Kingdom has overcome a soft power risk from temporary instability in late 2022 resulting from tumultuous government changes and the passing of Queen Elizabeth II. This year, the UK ranks 7th in ‘strong and stable economy’ compared to last year’s 12th and improves on ‘politically stable and well governed’ up to 12th from last year’s 16th. The nation’s Global Soft Power Index Score of 71.8 continues an upward trend from 67.3 in the previous year. Like the USA, as the UK is set for a general election this year, it will be interesting to see how the results impact its soft power.

China replaces Germany at the 3rd position in the soft power rankings, improving its overall score by +6.2, from 65.0 to 71.2 – faster than any other nation brand in the Global Soft Power Index this year. This rise is driven by a significant improvement in China’s perceptions across key Business & Trade and Education & Science metrics.

Germany fell to 5th position, after earning top ranking in 2021, and 3rd place in both 2022 and 2023. Germany has experienced stagnation and in many cases erosion in perceptions across the board this year, with a substantial drop of 14 positions in 'good relations with other countries' compared to 2023, along with decreases in helpful to countries in need' and measures of trustworthiness. Nevertheless, Germany achieved the top rank in Governance and, despite some score declines, remains among the leaders in the pursuit of a Sustainable Future.

India, Brazil, and South Africa struggle to fulfil their soft power potential, as all three nations have relatively high Familiarity and Influence, especially in their home regions, but rank lower for Reputation. India fell to 29th place, the highest ranked Latin American nation brand Brazil stagnated in 31st, and Sub-Saharan Africa ranking leader South Africa dropped to an all-time low in 43rd place.

With the ranking extended to cover all 193 member states of the United Nations, Monaco is the highest-ranked new entrant at 42nd. The world’s lowest-ranked nations are small Pacific Island nations Vanuatu (191st) Nauru (192nd) and Kiribati (193rd) - each limited in influence by population, geography, and economic factors.

Hard power harms soft power. Russia, Ukraine, and Israel have all ranked lower this year as respondents appear to downgrade countries engaged in military action. Russia continues to fall in soft power rankings, down three places to an all-time low of 16th. While Ukraine is down seven places to 44th, the nation continues to be ranked higher than at any time before Russia invaded. Israel has fallen five ranks to an all-time low ranking of 32nd.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.