New Brand Finance data shows US real estate brands are outperforming global peers, with brand values rising 13%

LONDON, 30 June 2026 - The global real estate sector continues to navigate a structurally shifting environment, with total brand value across the world’s top 50 real estate brands declining 14% to USD54.9 billion, according to the Real Estate 25 2026 report from Brand Finance, the world's leading brand valuation consultancy.

While transaction activity has recovered in parts of the market, performance remains highly uneven as capital concentrates in resilient, high-growth asset classes and technology-enabled operators.

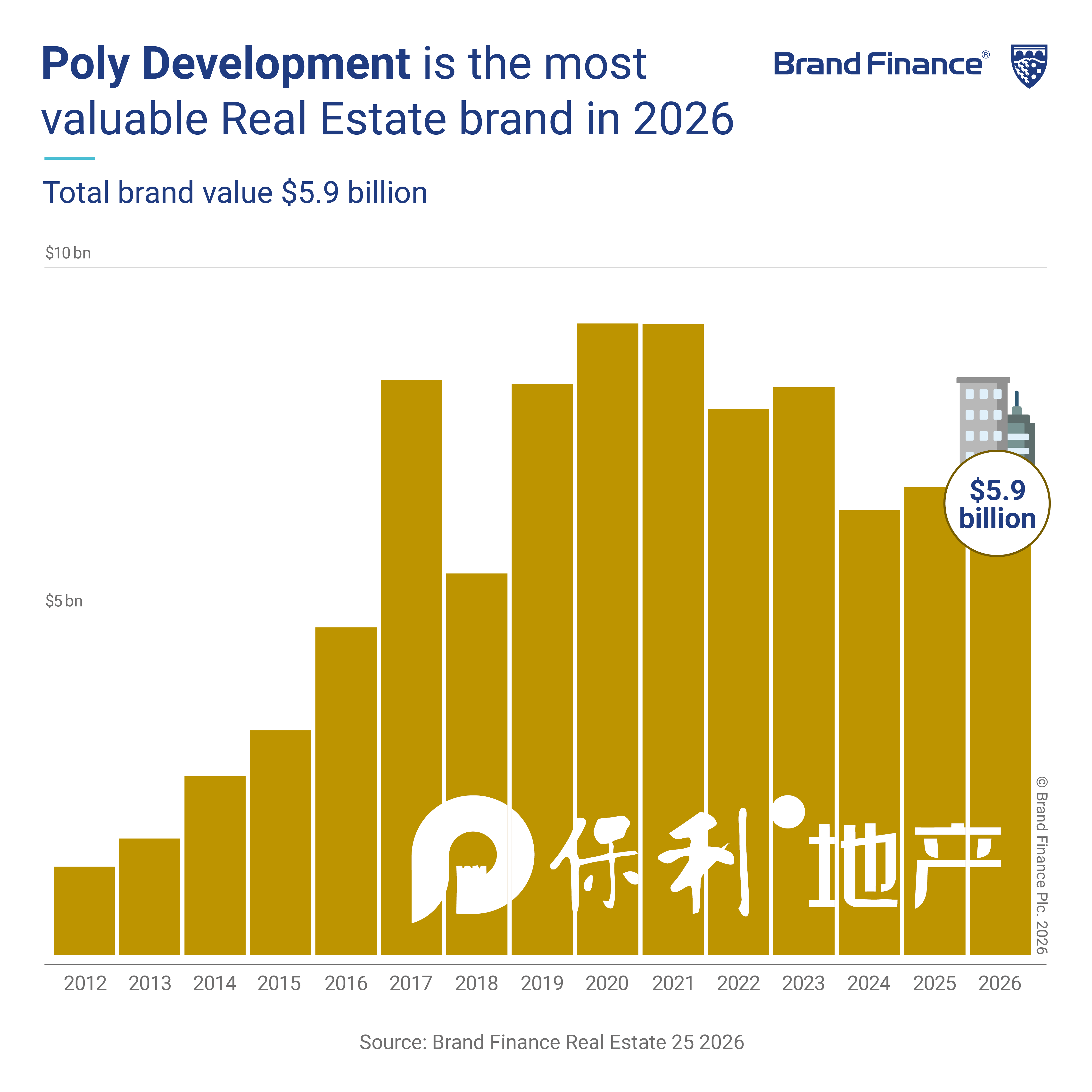

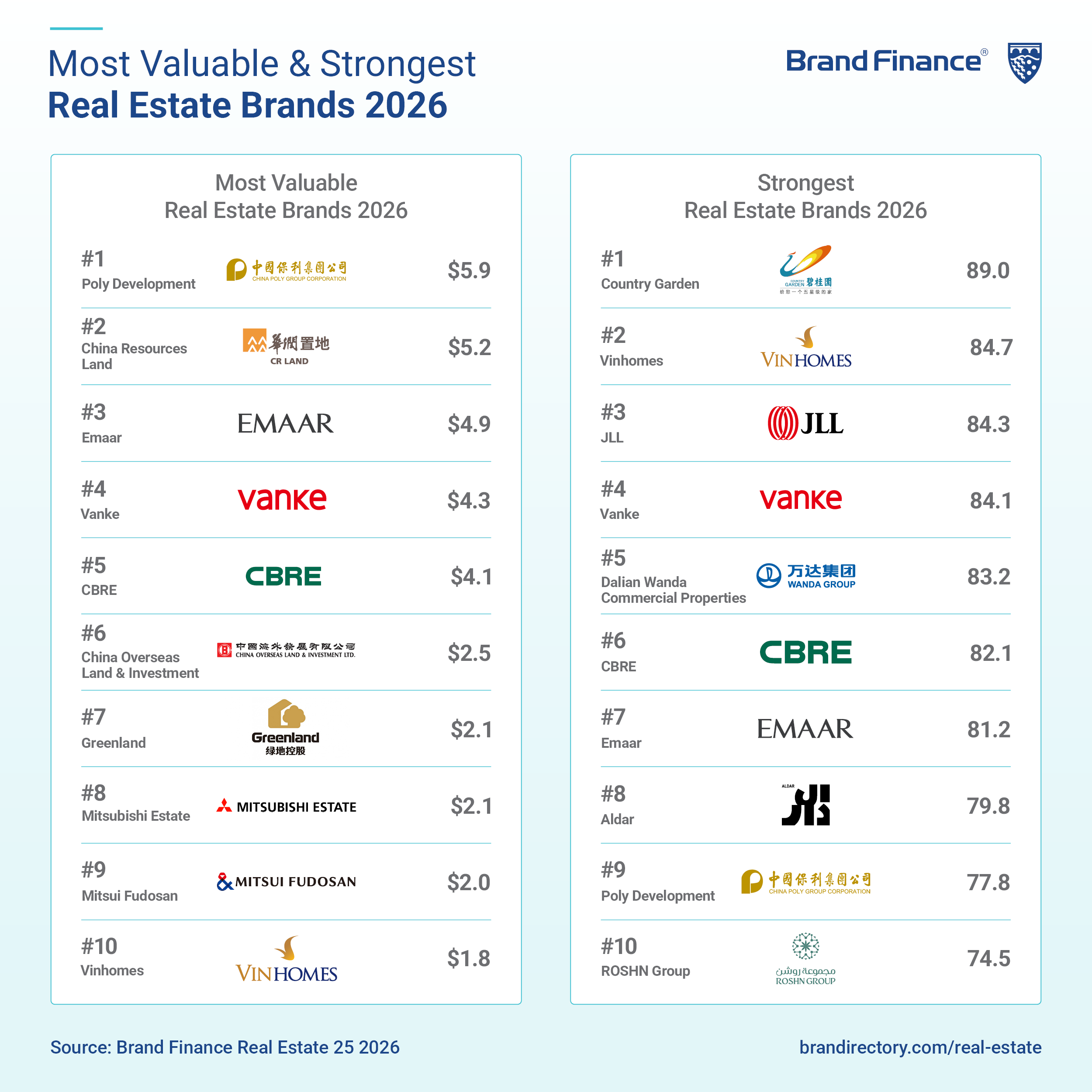

Despite sector-wide pressure, Poly Development emerges as the most valuable real estate brand in 2026 at USD5.9 billion, even as its brand value declines 12% amid continued weakness in China’s residential property market.

China Resources Land (brand value down 28% to USD5.1 billion) holds second place, reflecting stable rental income from commercial assets but weaker development sentiment. The brand's performance reflects the growing importance of maintaining investors and consumer confidence during periods of prolonged market uncertainty.

Emaar rises to third position with brand value growth of 21% to USD4.9 billion, recording one of the largest brand value growths in the sector. The Middle Eastern developer has managed market cycles by balancing performance across property, retail, and tourism.

Welltower emerges as the fastest-growing real estate brand globally, with its brand value surging 76% to USD1.7 billion. The brand's performance is driven by sustained strength in its senior housing portfolio, supported by favourable demographic trends and continued expansion of the “Silver Economy.” The brand’s Senior Housing Operating Portfolio (SHOP) delivered its 14th consecutive quarter of double-digit NOI growth, underpinned by rising occupancy levels and strong pricing power.

Alex Haigh, Global Sector Head of Real Estates, Brand Finance, commented:

“The 2026 real estate rankings demonstrate that brand strength has become an increasingly important differentiator in a complex and evolving market. Brands such as Poly Development, Welltower, Emaar, CBRE, and JLL illustrate how strong brands can create resilience, whether through scale, specialised market positioning, or long-term investment strategies. The sector’s leading performers are those that combine financial strength and operational excellence with the agility to respond to changing customer expectations, shifting market conditions, and evolving investment priorities.”

Host Hotels & Resorts (brand value up 17% to USD998 million) enters the Brand Finance Real Estate 50 rankings for the first time, marking it as a Brand to Watch. The brand’s inclusion in the ranking reflects the growing strategic importance of hospitality-linked real estate amid the recovery in global tourism and increasing demand for experience-driven assets. Strong operating performance in 2025, supported by higher room rates and resilient luxury travel demand, has reinforced investor confidence.

Despite significant financial pressure, Country Garden (brand value down 68% to USD1.3 billion) ranks as the strongest real estate brand globally, with a Brand Strength Index (BSI) score of 89/100 and an AAA brand strength rating. Its strength reflects high legacy awareness in China’s residential market, although perceptions of trust, delivery certainty, and financial stability remain under pressure following debt restructuring challenges.

Vinhomes (brand value up 13% to USD1.8 billion) ranks second in brand strength with a BSI of 84.7/100 and AAA brand strength rating, supported by strong domestic recognition but moderated by affordability perceptions and external sentiment linked to its broader corporate ecosystem.

JLL (brand value up 24% to USD1.6 billion) rises to third place with a BSI of 84.3/100 and AAA- brand strength rating, reflecting the resilience of professional services brands. Its strength is underpinned by research leadership, advisory credibility, and reduced exposure to cyclical development risk.

Meanwhile, the recovery in global commercial real estate brands continues to gather momentum, with transaction volumes stabilising and leasing demand improving across key asset classes. CBRE (brand value up 25% to USD4.1 billion) remains the most valuable commercial real estate services brand, while JLL (brand value up 24% to USD1.6 billion) is both the second most valuable and the strongest in the segment. Cushman & Wakefield (brand value up 8% to USD665 million) ranks third, recording steady growth, supported by improving leasing conditions and diversified service offerings.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.