View the full Brand Finance GIFT™ 2020 report here

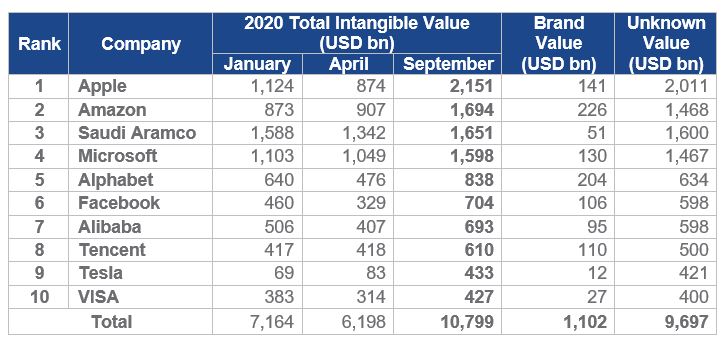

The Brand Finance Global Intangible Finance Tracker (GIFT™) study ranks the top global companies by total intangible value. The top 10 companies this year are Apple, Amazon, Aramco, Microsoft, Alphabet, Facebook, Alibaba, Tencent, Tesla, and VISA.

During the year, the intangible value of these companies started at US$7.2 trillion, then dropped by just shy of US$1 trillion during the COVID-19 crash, and finally skyrocketed to a total of US$10.8 trillion as at 1st September. This enormous volatility points to fundamental flaws in investor understanding of company assets.

Global stock markets have been extremely volatile in 2020 as a result of COVID-19, Brexit, a negative oil price, and the rollercoaster of Biden vs Trump. 2020 is considered to be the most volatile year since 1929, suggesting that most investors do not fully understand the underlying value of the companies they invest in, leaving room for wildly fluctuating share prices and mass panic.

The vast majority (97%) of the US$10.8 trillion of intangible value among the top 10 companies ranked in the Brand Finance GIFT™ 2020 study is undefined and remains undisclosed on company balance sheets. Brand Finance makes strides to narrow this disclosure gap by publishing the value of 5,000 of the world’s most valuable brands each year. Our brand values account for between 3% and 25% of the intangible value of these most intangible companies. The monetary value of other intangibles – technology, rights, relationships – remains unknown.

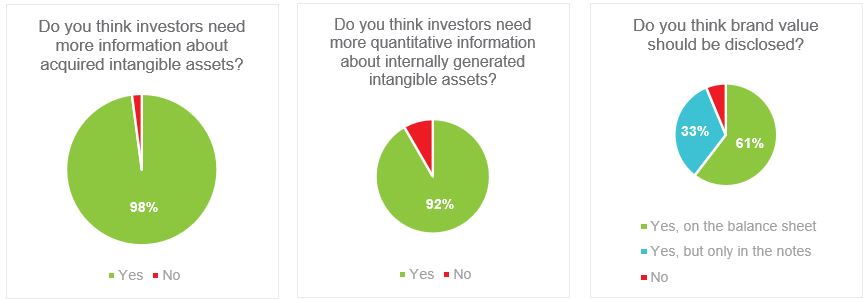

Brand Finance strongly believes that maintaining the status quo in financial reporting is simply irresponsible. Investors need more information about the nature and value of internally generated intangible assets. Brand Finance polled a representative sample of over 50 experts in the field asking if they agree – 92% think investors need more quantitative information about internally generated intangible assets.

This year, more than ever, has provided proof of the need for more comprehensive reporting of intangible asset value, to facilitate investor understanding and capital allocation.

To achieve this, reporting standards must demand more on the quality of intangible asset reporting. The IASB has launched a discussion paper on this very topic and will accept feedback for the next 10 weeks. Brand Finance encourages all stakeholders to engage in this topic, write to IASB, and demand better disclosure of intangible assets.

This is a once in a generation chance to alter the path of intangible asset reporting. Financial standards are only revisited every 15-20 years and there is a narrow window to effect change.

David Haigh, CEO of Brand Finance, commented:

“It is time for a revolution in financial reporting of intangible assets. I firmly believe that companies must do more to disclose the value of their most important assets. Intangibles play an increasing role in the modern economy – it is about time that balance sheets are allowed to reflect that.”

Annie Brown, Associate at Brand Finance, and author of the GIFT™ report, commented:

“Investors deserve better. They deserve better disclosure about internally generated intangibles, and they deserve a higher quality of the reporting of acquired intangibles. Reporting standards need to go further to guide boards to this greater transparency.”

View the full Brand Finance GIFT™ 2020 report here

Notes to Editors

Expert survey responses:

About Brand Finance GIFT™

The Brand Finance Global Intangible Finance Tracker (GIFT™) report is the world’s most extensive annual research exercise into intangible assets, considering over 59,000 publicly quoted companies (with a total value of over US$120 trillion) across 150 jurisdictions.

In its analysis, the Brand Finance GIFT™ 2020 report provides detailed insight into intangible value reporting by company, sector, and country. Consult the report document for graphs, additional insights, and opinion pieces by our experts.

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.