The World’s Most Valuable Brand– Amazon Breaks $200 Billion Mark

Tata Leads the Way for 11 Indian Brands in Global Ranking

View the full Brand Finance Global 500 2020 report here

Eleven Indian brands feature in the Brand Finance Global 500 report launching at the World Economic Forum in Davos today. Tata Group is the most valuable Indian brand in the ranking, with a brand value of US$20.0 billion. The bulk of Tata Group’s brand value comes from its IT services division TCS (up 5% to US$13.5 billion). TCS saw strong brand value growth on the back of increased performance of their artificial intelligence and cloud services, areas that are likely to continue growing strongly in the medium term. With the saturation of Internet of Things services requiring strong and trusted computing services to serve, store, and analyse devices, TCS is strongly placed to take advantage of the commercial opportunities. TCS is also the world’s third most valuable IT services brand in the Brand Finance IT Services 50 ranking.

Amazon breaks $200 billion mark

Defending its position as the world’s most valuable brand for the third consecutive year, Amazon has broken the so far unattainable US$200 billion brand value mark. Following 18% growth from US$187.9 billion last year, Amazon’s brand value has now reached US$220.8 billion, over US$60 billion more than Google’s and US$80 billion more than Apple’s.

The world’s largest online marketplace, Amazon has also branched out into cloud computing, artificial intelligence, consumer electronics, digital streaming, logistics, and is looking to enter other industries. With a diverse product and service portfolio, and thanks to continued investment in fast-growing sectors and innovative technologies, Amazon is not only the leader of today, but also seems primed for tomorrow.

Nevertheless, the majority of Amazon’s revenue still comes from retail, and challenges to the growth of the company’s core operations may result in brand value stagnation in the future. In November 2019, it was announced that Nike would no longer be selling its merchandise on the platform, to develop its own direct sales channels. Amazon may have to contend with other big brands following Nike’s lead, which would undermine its reputation as the ‘Everything Store’. Another potential sticking point is the future of Amazon’s international business. From environmentalist opposition in Europe, to backlash from local retailers in India, to saturation of China’s e-commerce market by Alibaba and its subsidiaries – matching globally the status that Amazon enjoys in the US, may prove difficult.

David Haigh, CEO of Brand Finance, commented:

“The disrupter of the entire retail ecosystem, the brand that boasts the highest brand value ever, Amazon continues to impress across imperishable consumer truths: value, convenience, and choice. Today, Amazon’s situation seems more than comfortable, but what will the roaring twenties hold in store?”

Digital can’t buy success

Forty-four retail brands feature in this year’s ranking alongside Amazon, with a combined value of nearly US$800 billion, making the sector the third most valuable behind tech and banking. As the boost from the novelty of operating in the digital space fizzles out, some online retailers have started to lose brand value, while bricks and mortar chains, which have learnt to successfully adapt to the changing marketplace, are consequently making gains.

In stark contrast to Amazon’s success, eBay’s brand value has continued to erode, falling 9% to US$8.2 billion. Despite the number of active buyers steadily increasing over the last year, reaching an impressive 183 million, eBay is failing to maintain relevance in an increasingly monopolised sector. Attempts to diversify and introduce new revenue streams, through eBay Payments and promoted listings, and potential spin offs in the pipeline, could mean the brand fares better in the coming year.

In the traditional retail space, American giant Walmart (up 14% to US$77.5 billion) has seen its brand value resurge, jumping up three places and entering the top 10 once again. As well as committing to its expansion programme in key markets, Walmart has focused on an innovative digital proposition, through a partnership with Microsoft and with the launch of Alphabot – robots that pick and pack online grocery orders at high speeds.

David Haigh, CEO of Brand Finance, commented:

“Despite the unprecedented disruption caused by e-commerce, the popular assertion that entering digital operations brings instant success while bricks and mortar stores are doomed for extinction is being proved wrong. As digital operators find they need to remain attentive to consumers and traditional retailers, such as Walmart, successfully adapt to change, we are back to normal as all players realise that ultimately the customer is king.”

Mirroring the situation in retail, many traditional hoteliers are seeing significant growth this year, while brands operating in the digital space see mixed results. Hilton Hotels & Resorts remains the sector’s top brand and one of the fastest-growing brands in the ranking overall, improving its brand value 35% to US$10.8 billion, thanks to marrying experience with a clear vision for growth. Although still trailing Hilton, Marriott has also seen substantial growth over the past year, recording a 20% uptick to US$6.0 billion. Their pace of brand value growth is comparable to Airbnb’s, up 28% to US$10.5 billion, while another digital player – Booking.com – saw a 15% decline to US$10.2 billion this year.

Brand bubble bursting?

Despite many success stories, there are also clear signs of a slowdown. The combined value of the Brand Finance Global 500 has increased by less than 2% year on year, and while 244 brands have increased their brand value, another 212 are down, including 95 by 10% or more. Those which once enjoyed long-term success are now needing to adjust in a world more unpredictable than ever, while many tech brands are suffering after failing to meet the bullish expectations of investors.

This is true of Chinese software giant Baidu which recorded the largest drop in brand value, down 54% to US$8.9 billion. The company reported its first quarterly loss since its initial public offering (IPO) back in 2005. Along with intense market competition, the brand’s revenues were heavily impacted as regulators placed more attention on online advertising. Baidu is now focusing on other areas to drive long-term growth, such as its cloud division, smart speakers, and even driverless cars in an effort to secure better results for the future.

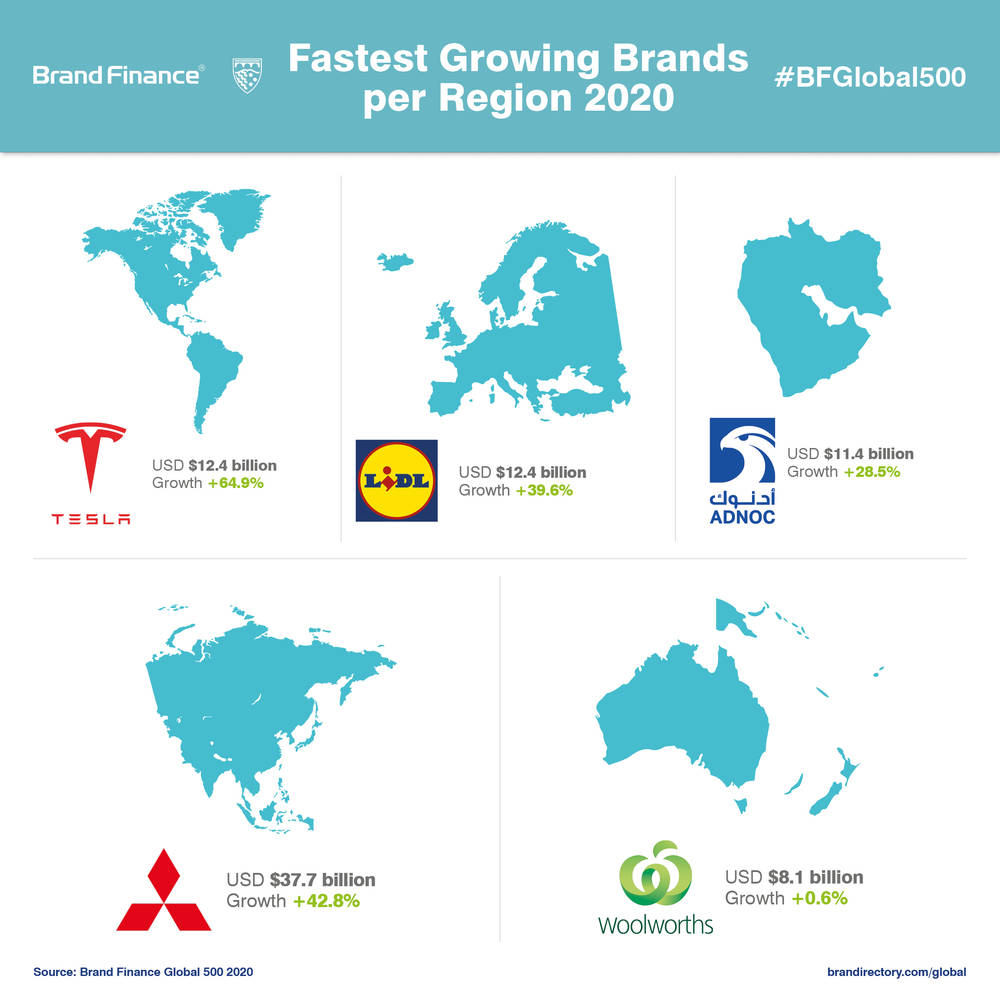

In contrast, one company still very much on the road to success is Tesla, racing ahead as the fastest-growing brand with a brand value of US$12.4 billion, up 65% on last year’s valuation. The electric vehicle innovator began sales to customers in further reaches than ever before, including China, Australia, the UK, and several markets in Eastern Europe. Although there have been concerns of achieving production targets, the brand appears to be living up to its hype and is growing in value and strength.

Excitement alone, though, cannot carry a brand – it must deliver on its promise, something Uber is battling to do as its brand value dropped by one third, down 32% to US$15.3 billion, forcing it to share the ride with five fastest-falling brands in the ranking. The company went public this year but with disappointing results, closing its first day of trading with a 7.6% reduction in valuation. Uber continues to take hits, including the loss of its license to operate in London after repeated safety failures. Reminded by investors of the old adage that ‘revenue is vanity, profit is sanity, cash is reality ‘, the company is trying to get back on track and reorganised its internal structure, with a prioritisation on efficiency, profitability, and positive cashflow.

Unlike apps which have not been able to satisfy expectations, Instagram is enjoying an explosion of growth, securing the second-highest brand value increase this year, up 58% to US$26.4 billion. With more than 1 billion active monthly users and a focus on new technology, like the latest Checkout feature that benefits both consumers and other brands, Instagram is catering to demand and staying relevant.

David Haigh, CEO of Brand Finance, commented:

“Twenty years on from the dot-com bubble, as we witness global slowdown and the failure of hyped IPOs from WeWork to Uber, we may be only months away from the startup bubble bursting right in our faces. When expectation and reality do not match, the truth will out and the results can be devastating. The cost of capital is increasing, putting breaks on indefinite brand value growth, and a shift from a startup bidding war towards appraising real value is necessary.”

Telecoms call for help

A call to the help desk may be in order for the telecoms industry, as the majority of brands – 4 out of 5 – saw their brand value decline this year, despite strong investments. Over the past five years, the combined value of telecoms brands in the Brand Finance Global 500 has stagnated, while all other major sectors recorded significant increases. Big telcos are being squeezed from all sides as OTT messaging apps like WhatsApp are impacting voice and SMS revenue, and challenger brands offer comparable data services at below-market rates, leading to fierce price competition and decreasing margins.

US giant AT&T is the fastest-falling telecoms brand this year, down 32% to US$59.1 billion. Just like its biggest rival Verizon, AT&T finds itself outside of the top 10 most valuable brands in the world for the first time in nearly a decade. The company diversified its entertainment portfolio over the last few years, culminating with the acquisition of WarnerMedia, part of a plan to move away from reliance on the traditional telco business and pay television, as both revenue streams have been drying up. AT&T recently announced a plan to drive significant growth through 2022, including investing in strategic areas, such as 5G infrastructure enabling innovative services far above and beyond internet data.

Clearly the next big opportunity for the telecoms industry, the 5G space is inviting fierce competition, with Huawei expanding into markets traditionally covered by Western providers. Despite sparking controversy, the Chinese giant is making clear headway, and with a brand value of US$65.1 billion, now counts among the world’s top 10 most valuable brands for the first time.

David Haigh, CEO of Brand Finance, commented:

“It is not surprising that a number of telco brands have placed bets on new opportunities from video content rights to Internet of Things ventures. Focus on extracting as much value as possible from the declining segments cannot sustain growth in the long term, as the consumption of telecommunications has changed for good. AT&T is the perfect example of how to fight back against the shrinking of the traditional market as they lead the charge in 5G – an area ripe for expansion.”

Saudi Aramco strikes oil

With a brand value of US$46.8 billion, Saudi Aramco is the most valuable among the 44 new entrants in the ranking. The publication of the Saudi Arabian oil and gas company’s financials at the time of the IPO allowed for its brand to be included in Brand Finance’s annual study for the first time. Placing 24th globally, Saudi Aramco also claims the title of the most valuable brand in the Middle East and Africa.

The IPO has proven to be successful for the brand as Saudi Aramco raised US$25.6 billion, making it the largest ever to date. Even after navigating through recent attacks on two of its oil processing sites, it is now the world’s most valuable listed company, comfortably ahead of tech titans Apple and Microsoft. Saudi Aramco is focused on leveraging its strength in upstream, while growing its downstream operations through acquisitions, both in Saudi Arabia and key global markets. The company must now focus on developing international perceptions of the brand in order to open it up further for partnerships and investment.

Ferrari in pole position again

For the second year in a row, Ferrari, the iconic Italian luxury sports car manufacturer, has retained its position as the world’s strongest brand with a Brand Strength Index (BSI) score of 94.1 out of 100. Brand Finance determines the relative strength of brands through a balanced scorecard of metrics evaluating marketing investment, stakeholder equity, and business performance. According to these criteria, Ferrari is the strongest of only 12 brands in the Brand Finance Global 500 2020 ranking to have been awarded the highest AAA+ rating.

Alongside revenue forecasts, brand strength is a crucial driver of brand value. As Ferrari’s brand strength maintained its rating, its brand value grew, improving 9% to US$9.1 billion. Ferrari announced five new models in 2019 and established a manufacturing agreement with the Giorgio Armani Group to help push Ferrari collections into a more premium space. For years, Ferrari has utilised merchandise to support brand awareness and diversify revenue streams, and are now taking steps to preserve the exclusivity of the brand.

“The embodiment of luxury, Ferrari continues to be admired and desired around the world, and its outstanding brand strength reflects this. It is no wonder that many consumers, who might never own a Ferrari car, want a bag or a watch emblazoned with the Prancing Horse, but it is also crucial that the company management remain at the steering wheel of the brand’s future and maintain its exclusive positioning by monitoring the licensing output closely.”

View the full Brand Finance Global 500 2020 report here

ENDS

Note to Editors

Every year, leading independent brand valuation consultancy Brand Finance values the world’s biggest brands. The world’s 500 most valuable brands across all sectors and countries are included in the Brand Finance Global 500 2020 report.

The 2020 iteration of the Brand Finance Global 500 report was launched today at the World Economic Forum in Davos, Switzerland.

Brand value is understood as the net economic benefit that a brand owner would achieve by licensing the brand in the open market. Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors.

Additional insights and charts, more information about the methodology, as well as definitions of key terms are available in the Brand Finance Global 500 2020 report.

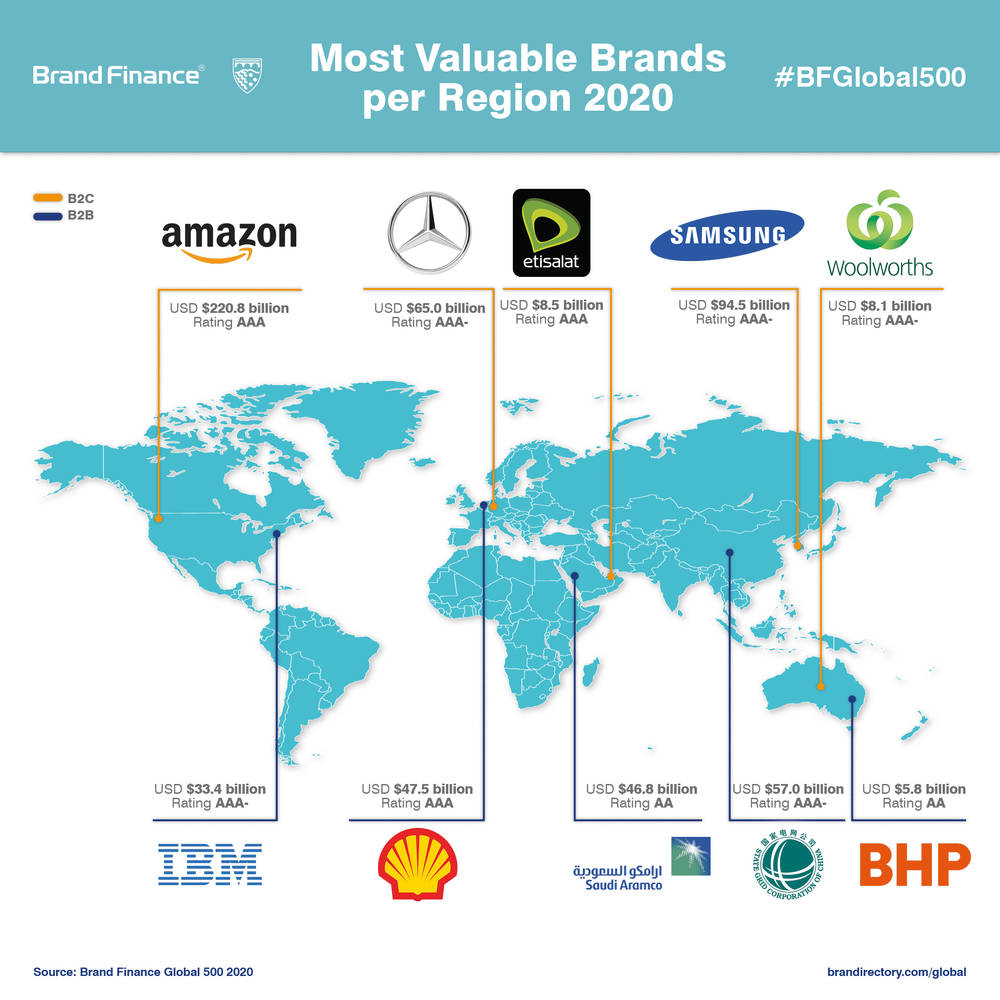

Please click here for an infographic on the most valuable B2C and B2B brands by region and an infographic on the fastest-growing brands per region included in the report.

Brand Finance helped craft the internationally recognised standard on Brand Valuation – ISO 10668, and the recently approved standard on Brand Evaluation – ISO 20671.

Data compiled for the Brand Finance league tables and reports are provided for the benefit of the media and are not to be used for any commercial or technical purpose without written permission from Brand Finance.

Media Enquiries

Konrad Jagodzinski

Communications Director

T: +44 (0)2073 899 400

M: +44 (0)7508 304 782

k.jagodzinski@brandfinance.com

WEF 2020 Davos Media Enquiries

Sehr Sarwar

Communications Director

M: +44 (0)7966 963 669

s.sarwar@brandfinance.com

Follow us on Twitter @BrandFinance #BFGlobal500 and LinkedIn.

About Brand Finance

Brand Finance is the world’s leading independent brand valuation consultancy, with offices in over 20 countries. Brand Finance bridges the gap between marketing and finance by quantifying the financial value of brands. Drawing on expertise in strategy, branding, market research, visual identity, finance, tax, and intellectual property, Brand Finance helps brand owners and investors make the right decisions to maximise brand and business value.

Methodology

Definition of Brand

Brand Finance helped craft the internationally recognised standard on Brand Valuation – ISO 10668. It defines a brand as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand Strength

Brand strength is the efficacy of a brand’s performance on intangible measures, relative to its competitors. In order to determine the strength of a brand, we look at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding rating up to AAA+ in a format similar to a credit rating.

Brand Valuation Approach

Brand Finance calculates the values of the brands in its league tables using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

Downloads

Brand Finance is the world’s leading brand valuation consultancy. Bridging the gap between marketing and finance, Brand Finance evaluates the strength of brands and quantifies their financial value to help organisations make strategic decisions.

Headquartered in London, Brand Finance operates in over 25 countries. Every year, Brand Finance conducts more than 6,000 brand valuations, supported by original market research, and publishes over 100 reports which rank brands across all sectors and countries.

Brand Finance also operates the Global Brand Equity Monitor, conducting original market research annually on 6,000 brands, surveying more than 175,000 respondents across 41 countries and 31 industry sectors. By combining perceptual data from the Global Brand Equity Monitor with data from its valuation database — the largest brand value database in the world — Brand Finance equips ambitious brand leaders with the data, analytics, and the strategic guidance they need to enhance brand and business value.

In addition to calculating brand value, Brand Finance also determines the relative strength of brands through a balanced scorecard of metrics, compliant with ISO 20671.

Brand Finance is a regulated accountancy firm and a committed leader in the standardisation of the brand valuation industry. Brand Finance was the first to be certified by independent auditors as compliant with both ISO 10668 and ISO 20671 and has received the official endorsement of the Marketing Accountability Standards Board (MASB) in the United States.

Brand is defined as a marketing-related intangible asset including, but not limited to, names, terms, signs, symbols, logos, and designs, intended to identify goods, services, or entities, creating distinctive images and associations in the minds of stakeholders, thereby generating economic benefits.

Brand strength is the efficacy of a brand’s performance on intangible measures relative to its competitors. Brand Finance evaluates brand strength in a process compliant with ISO 20671, looking at Marketing Investment, Stakeholder Equity, and the impact of those on Business Performance. The data used is derived from Brand Finance’s proprietary market research programme and from publicly available sources.

Each brand is assigned a Brand Strength Index (BSI) score out of 100, which feeds into the brand value calculation. Based on the score, each brand is assigned a corresponding Brand Rating up to AAA+ in a format similar to a credit rating.

Brand Finance calculates the values of brands in its rankings using the Royalty Relief approach – a brand valuation method compliant with the industry standards set in ISO 10668. It involves estimating the likely future revenues that are attributable to a brand by calculating a royalty rate that would be charged for its use, to arrive at a ‘brand value’ understood as a net economic benefit that a brand owner would achieve by licensing the brand in the open market.

The steps in this process are as follows:

1 Calculate brand strength using a balanced scorecard of metrics assessing Marketing Investment, Stakeholder Equity, and Business Performance. Brand strength is expressed as a Brand Strength Index (BSI) score on a scale of 0 to 100.

2 Determine royalty range for each industry, reflecting the importance of brand to purchasing decisions. In luxury, the maximum percentage is high, while in extractive industry, where goods are often commoditised, it is lower. This is done by reviewing comparable licensing agreements sourced from Brand Finance’s extensive database.

3 Calculate royalty rate. The BSI score is applied to the royalty range to arrive at a royalty rate. For example, if the royalty range in a sector is 0-5% and a brand has a BSI score of 80 out of 100, then an appropriate royalty rate for the use of this brand in the given sector will be 4%.

4 Determine brand-specific revenues by estimating a proportion of parent company revenues attributable to a brand.

5 Determine forecast revenues using a function of historic revenues, equity analyst forecasts, and economic growth rates.

6 Apply the royalty rate to the forecast revenues to derive brand revenues.

7 Discount post-tax brand revenues to a net present value which equals the brand value.

Brand Finance has produced this study with an independent and unbiased analysis. The values derived and opinions presented in this study are based on publicly available information and certain assumptions that Brand Finance used where such data was deficient or unclear. Brand Finance accepts no responsibility and will not be liable in the event that the publicly available information relied upon is subsequently found to be inaccurate. The opinions and financial analysis expressed in the study are not to be construed as providing investment or business advice. Brand Finance does not intend the study to be relied upon for any reason and excludes all liability to any body, government, or organisation.

The data presented in this study form part of Brand Finance's proprietary database, are provided for the benefit of the media, and are not to be used in part or in full for any commercial or technical purpose without written permission from Brand Finance.

{kind=link}

{kind=link}

{kind=link}