This article was originally published in the Brand Finance Banking 500 Journal 2026.

Across markets, there is a growing sense that the world has become harder to interpret. People are dealing with more information, more rapidly, within an environment that feels increasingly unsettled. Political tensions are emerging in new places, economic pressures continue to weigh on households, and social divisions are becoming more pronounced. Environmental risks are intensifying, and questions about resources are becoming a regular part of public debate. At the same time, technology is once more reshaping how information is produced and circulated, making it harder than ever to judge what is reliable.

All this taken together has left many people feeling as though long-standing points of stability are no longer as dependable as they once were. The latest Global Risks Report from the World Economic Forum also identifies misinformation and disinformation among the leading short-term global risks, under scoring how fragile trust in information and in the institutions that provide it has become.

This creates an opportunity for businesses, especially financial services brands as they are related to people’s financial security today and in the future, from mortgages, savings, business loans and pensions, all woven into life’s milestones. Brands that deliver reliably, act with transparency and respond to the issues people care about can provide a sense of stability when it is most needed. In doing so, they build stronger relationships with stakeholders and strengthen their resilience in a more demanding environment.

How trust is built - A simple framework for brands

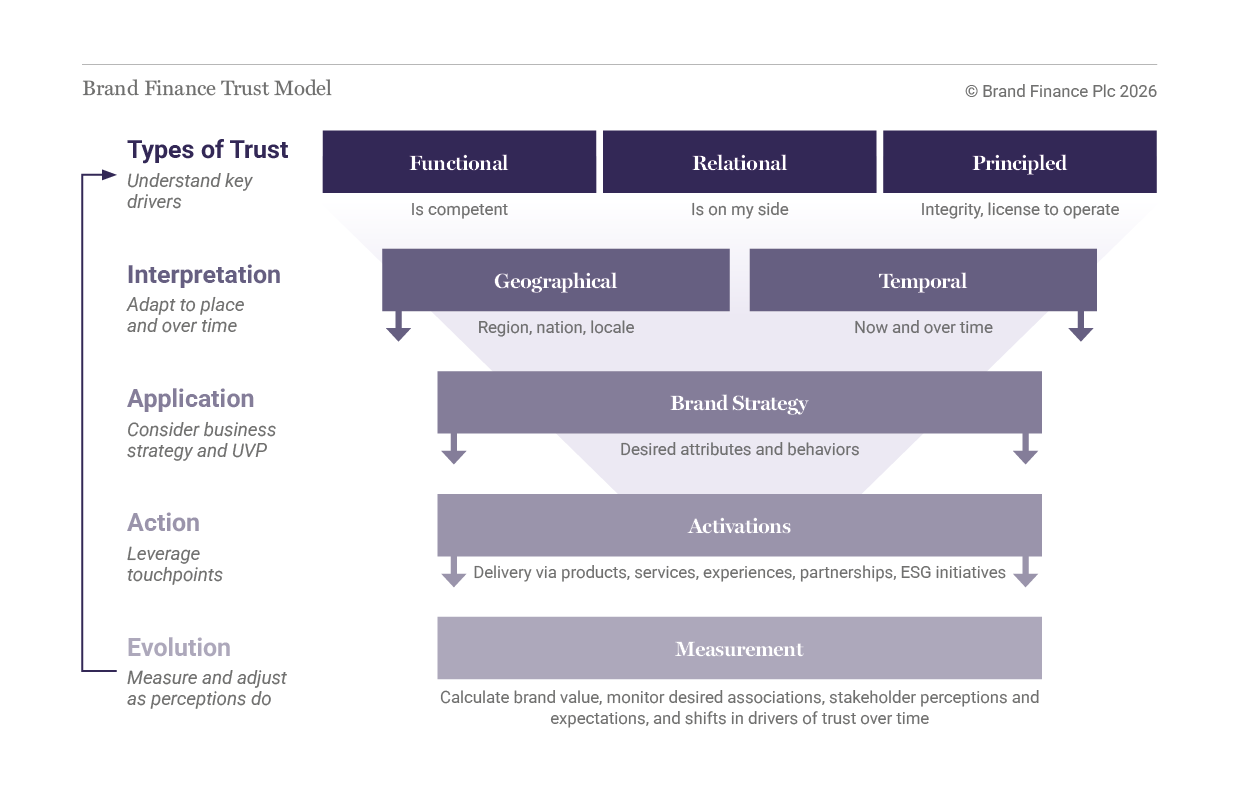

Our research at Brand Finance shows that trust is built on three interconnected pillars: functional performance, relational experience and integrity.

Functional trust forms the foundation. Customers need to believe their bank is competent, secure and financially sound. In an increasingly digital banking environment, this means systems that work seamlessly, data that is protected against cyberattacks, and services that are consistently reliable. When platforms fail or processes feel opaque, confidence erodes quickly. Conversely, when performance is steady and predictable, banks provide something people deeply value in uncertain times: stability.

But competence alone is not enough. Relational trust reflects how customers feel they are treated. Do they feel supported when facing financial pressure? Are communications clear rather than confusing? Is service responsive rather than transactional? Especially during periods of economic strain, the human dimension of banking becomes more visible. Customers may forgive occasional friction, but they are less forgiving of indifference.

Modelling our research data to see how these pillars differ by region adds important nuance. Across most regions, functional performance is an entry ticket: security, reliability and systems that work smoothly are essential and failure here can mean banks are not even considered. Once this baseline is met, markets diverge.

In Western markets, relational experience tends to matter more than reputational or principled cues. These are the day-to-day “how am I treated” factors such as responsiveness, ease and fairness.

Meanwhile, in the Middle East, APAC and LATAM, reputational and principled attributes carry more weight. Here, trust is anchored less in “did that interaction feel good?” and more in “is this institution fundamentally dependable?”.

The third pillar, integrity, has become increasingly decisive: Brand Finance research shows that integrity-related attributes drive around 9% of brand consideration in the banking sector. Stakeholders expect transparency, fairness and accountability, from pricing transparency to responsible lending, from governance standards to the ethical use of customer data. Integrity signals that a bank is not only capable, but principled. In an era where scepticism towards institutions is widespread, this perception can materially influence brand strength.

But trust does not look identical everywhere. Geography, culture, personal upbringing, economic context, regulatory environments and issues dominating public conversation all shape what people look for. For international banking brands, this means that while the three pillars of trust remain consistent, the brand expression might need to adapt.

Structural Equation Modelling (SEM) helps to quantify how different aspects of a brand’s image influence outcomes such as consideration, usage, advocacy and price premium acceptance. Signals of quality or distinctiveness tend to be powerful drivers of consideration, while the attributes people associate with trust often play a meaningful role in price acceptance and loyalty. The precise mix varies by category and market, but the pattern is consistent: what people believe about a brand materially affects how they behave to wards it.

However, touchpoints contribute to these perceptions unevenly. Some channels and experiences build positive associations reliably, while others have limited or even counterproductive effects depending on the sector. For example, our modelling in the luxury sector shows that more direct forms of interaction often have a stronger influence on trust-related perceptions than broader messaging channels, and this might also be the case for premium and private banking clients.

Understanding these variations is essential, because it highlights where investment supports long-term brand strength and brand value creation, and where it may unintentionally erode it.

What does this mean for banks in 2026?

People are looking for reassurance in a world that feels increasingly uncertain. Brands that under stand what drives trust – and how it influences be haviour – are better placed to offer people a sense of steadiness amid this uncertainty, building stronger relationships with their stakeholders and generating lasting business value.

For banks it means first that functional excellence is non-negotiable. Seamless digital experience and cybersecurity are basic requirements rather than differentiators.

Second, technology must enhance, not dilute, the relational experience. As automation and use of AI increases, empathy when interacting with customers becomes more important.

Finally, integrity must be visible.

Transparent communication and responsible conduct reinforce credibility over time, but also to what extent financial services institutions are engaging in corporate responsibility initiatives, such as those which foster financial literacy.

Trust has become more valuable precisely because it is harder to earn, and it shifts as expectations, contexts and experiences change.

The organisations that invest in delivering high-quality products and services, anchored in understanding and addressing customers’ needs with fairness, respect and excellence, alongside clarity, consistency and responsible action will be the ones best equipped to restore confidence and strengthen their position as trust becomes a defining factor in competitive advantage and value creation.