In January 2018, news headlines resounded with the announcement of the UK’s biggest trading liquidation to date. Carillion’s bankruptcy destroyed jobs and further destabilised confidence in the UK economy.

But the downfall was not a complete surprise to the hedge-funds that made £200 million by short-selling shares in Carillion. A review of Carillion’s performance in the GIFT™ 2018 study also indicates that downfall was more inevitable than shocking. A closer examination of historic disclosure of goodwill illuminates a worrying indicator that Carillion’s collapse may have been years in the making. What remains in the construction mammoth’s wake is a stark cautionary tale about heavy M&A and the improper accounting of goodwill.

How Did This Happen? Fair Value Exercises and Acquisitions

When one company is bought by another, a fair value exercise (FVE) must take place to allocate the consideration paid to net tangible assets and identifiable intangible assets. Any remaining unallocated value is classified as goodwill.

Since 2001, the IASB has adopted the policy that goodwill identified upon the acquisition of a company will subsequently be accounted for through impairments and not annual amortisation. This policy contends that goodwill does not necessarily decrease in value as time goes on.

However, it can also allow persistent high levels of goodwill on company balance sheets, the reported value of which is dependent on management judgment. Where neither managers nor auditors feel an impairment is due, no impairment charge is taken against the carrying amount of the goodwill asset. In extreme cases, persistent non-impairment can inflate the balance sheet, leaving investors, employees and entire economies vulnerable.

Real Impairment vs. Reality

Our Global Intangible Finance Tracker (GIFT™) study compares this distribution of asset value. We identify the value of listed companies’ tangible net assets, disclosed goodwill and other disclosed intangibles (such as brand value) present on their balance sheets. The sum of these three disclosed items is then compared with the companies’ market enterprise values. The balancing figure is allocated to undisclosed intangible value.

This undisclosed value is the excess of market value over book value created through changing share price. Share prices fluctuate due to changing expectations of future earnings, which are driven by signals on future performance, such as innovative technology, the popularity of the brand, and announcements of new contractual agreements, which are examples defined under IAS 38 as intangible assets.

When undisclosed intangible value is negative, book value exceeds market value, indicating real economic impairment.

Goodwill recognised in a business combination is an asset representing the future economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognised. The future economic benefit may result from synergy between the identifiable assets acquired or from assets that, individually, do not qualify for recognition in the financial statements.

IAS 38

Our GIFT™ 2018 study found 1,215 publicly traded companies domiciled in countries which use IFRS and had negative undisclosed intangible value for both financial years 2017 and 2016. In our view, this indicates the need for impairment of goodwill. However, 70% of these companies had either no reduction or an increase in disclosed goodwill over these two years, which can be treated as a proxy for non-impairment.

One would expect that companies with a more significant value of goodwill if exercising prudence, would be more likely to impair when economic goodwill impairment is indicated. We tested this hypothesis. Surprisingly, we found very little relation between the ratio of goodwill to market enterprise value and propensity to impair. 69% of companies with the ratio at 10% or less did not impair, compared with 70% of companies with the ratio at more than 100%.

When a firm has been acquiring aggressively and thus has accrued significant amounts of goodwill, it would not be unusual to have high levels of goodwill relative to market enterprise value. However, if those acquisitions are strategically weak, and the benefits of expected synergies are not realised, then goodwill would be a high proportion of market value over a longer-term. This would indicate an inflated balance sheet as the expected earnings that determine goodwill do not prove true in time.

When this goodwill is not impaired, the balance sheet and retained earnings are likely overstated, reducing the reliability of financial statements. Even if the initial recognition of goodwill is accurate, subsequent non-impairment can be misleading and harmful to investors. Management is incentivised not to impair; it reflects badly on the incumbent CEO as it suggests they may have overpaid for an acquisition. Often it is new executives that initiate impairment; for example on the day that GE introduced Larry Culp as CEO, the company announced a US$23 billion goodwill impairment.

The Construction Mammoth and the Elephant in the Balance Sheet

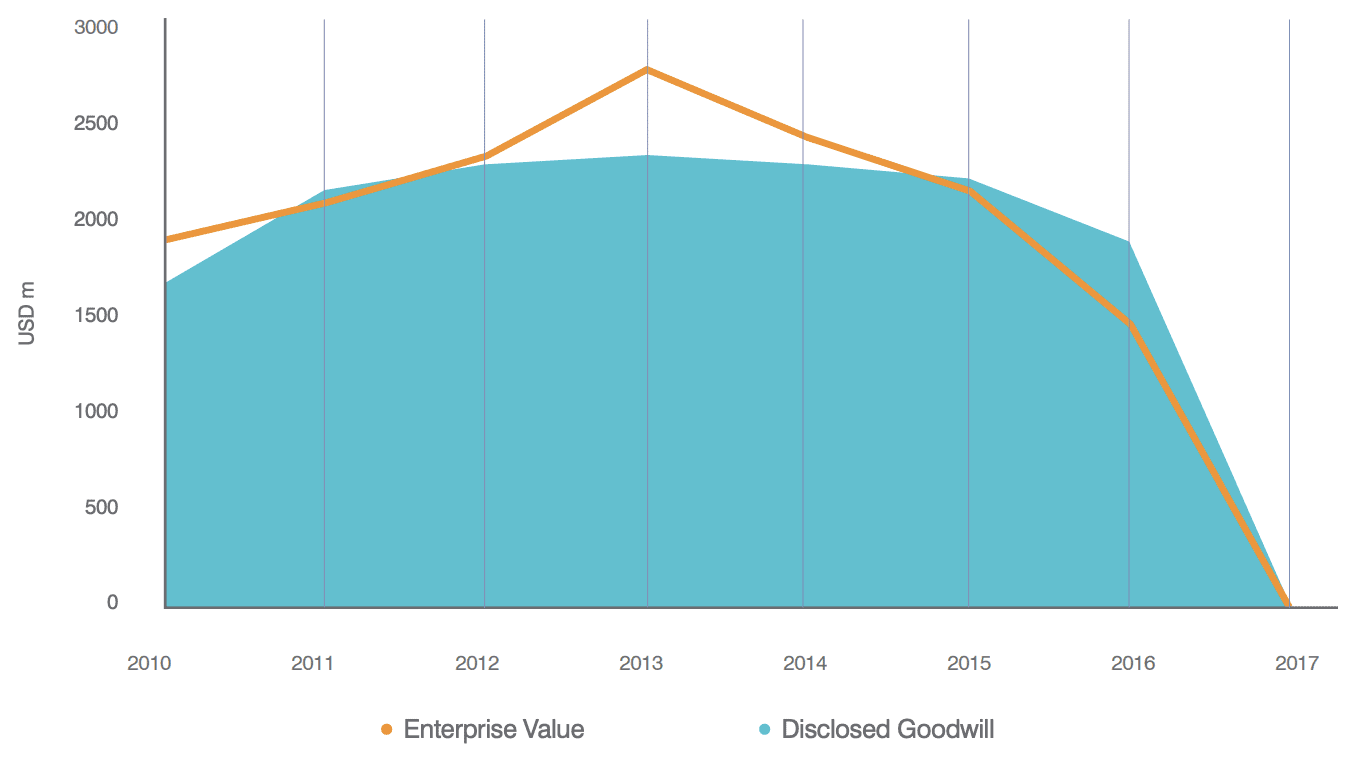

Many critics cite Carillion’s subsidiary Eaga as the main problematic treatment of group acquired goodwill. While it was substantial at £329 million, Eaga contributed to just 19% of Carillion’s disclosed goodwill. Since 2011, disclosed goodwill accounted for at least 84% of Carillion’s market enterprise value, and in the years 2012, 2016, and 2017, the book value of goodwill even exceeded the total market worth of the company.

Consider that the average share of market enterprise value disclosed as goodwill for the global set of trading companies between 2011-2017 was a mere 6% and join the critics of KPMG that wonder why goodwill was not impaired.

KPMG conducted a sensitivity analysis on the earnings forecasts and valuation assumptions for the relevant CGUs and concluded that no impairment was necessary. However, a sensitivity analysis is only reliable when the forecasts are approximately correct. Eaga, which was rebranded to Carillion Energy Services (“CES”), had suffered a decrease in revenue of 95% in the five years after acquisition.

This decrease in performance should have indicated that future earnings may be lower than originally expected, which would imply goodwill should be impaired. However, in this five-year period, no impairment was charged against the goodwill that arose on acquisition.

To be fit for purpose, a balance sheet must present a true and fair view of the reporting entity’s financial position. This relies heavily on auditors’ diligence surrounding the figures provided by management. This diligence is often lacking.

In the case of Carillion, despite a weakened financial outlook, no impairment charges were elicited by management or the auditors. As goodwill impairment is an expense against retained earnings, it can eliminate the reserves from which dividends are paid. Because of non-impairment, Carillion was able to pay out a record amount of £78 million in dividends in 2016.

Prudence. Prudence. Prudence.

If, unlike so far assumed in this article, goodwill on acquisition is inaccurate, then either:

- The high value of goodwill demonstrates that management overpaid for the target company, or

- Management did not overpay, but the allocation of intangible value is inaccurate, and the value of other specific intangible assets acquired, such as brand, are underestimated.

Under both scenarios, it would be understandable for the carrying amount of goodwill to then be improperly impaired, given that CEOs don’t like to admit to having overpaid for an acquisition. However, both scenarios could be avoided if specific intangible assets are more accurately valued.

Goodwill is neither transparent nor understandable. Other intangibles, such as brands and software are easier for investors to interpret. For example, a major scandal would signal that brand value should be impaired. Goodwill, on the other hand, is more obscure, making impairment less obvious.

On the acquisition of Eaga, Carillion rebranded it to CES. Had the FVE accounted for the brand value of Eaga, such a rebrand would have likely resulted in the impairment of this brand value immediately. However, the only intangible asset separated in the FVE was customer contracts and lists, which were recognised at £29.4 million, and amortised completely over 4 years. This value is just 9% of what was recognised as goodwill.

Brands Can Live Forever

Managers are incentivised to allocate as much intangible value to goodwill as possible, to minimise amortisation expenses. Granted, the allocation of purchase-price to specific assets instead of goodwill can sometimes result in lower earnings due to amortisation charges. But if the useful economic life is determined by expert independent parties, this amortisation should be more accurate of economic amortisation and impairment than under the current model.

In addition, in some cases, intangible assets can have an indefinite useful economic life; the implications of which are three-fold. Firstly, the original fair value attributed to the intangible asset will be higher since their longer life will make them more valuable. Secondly, there will be no amortisation charges required against these assets – as, with goodwill, only impairment testing is required. Thirdly, goodwill on acquisition will be suppressed. Unlike with goodwill, specific intangible assets, such as brands, are more transparent – they are implicitly more understandable. Therefore, an auditor is held more accountable to external indicators of impairment.

Fair Value to All

One could argue that reallocating goodwill to other intangible assets is too costly to justify and serves no use since impairment is still not charged. However, an accurate understanding of specific intangibles is useful, relevant and increasingly material. To ensure that designation of useful economic life and fair market value are accurate, an objective and transparent valuation is required.

In 2016, we partnered with the Institute of Practitioners in Advertising (IPA) to survey equity analyst and CFO opinions on this matter. We found that the majority (58% of analysts and 46% of CFOs) think that independent third-party intangible asset valuers should prepare the valuations of intangible assets included in financial accounts. While this would increase the reliability of intangible assets, there would likely remain some goodwill.

If goodwill is accurate – only reflective of excess earnings due to synergies, and these future earnings are achieved – then as earnings grow post-acquisition, a constant level of goodwill should represent a decreasing proportion of business value.

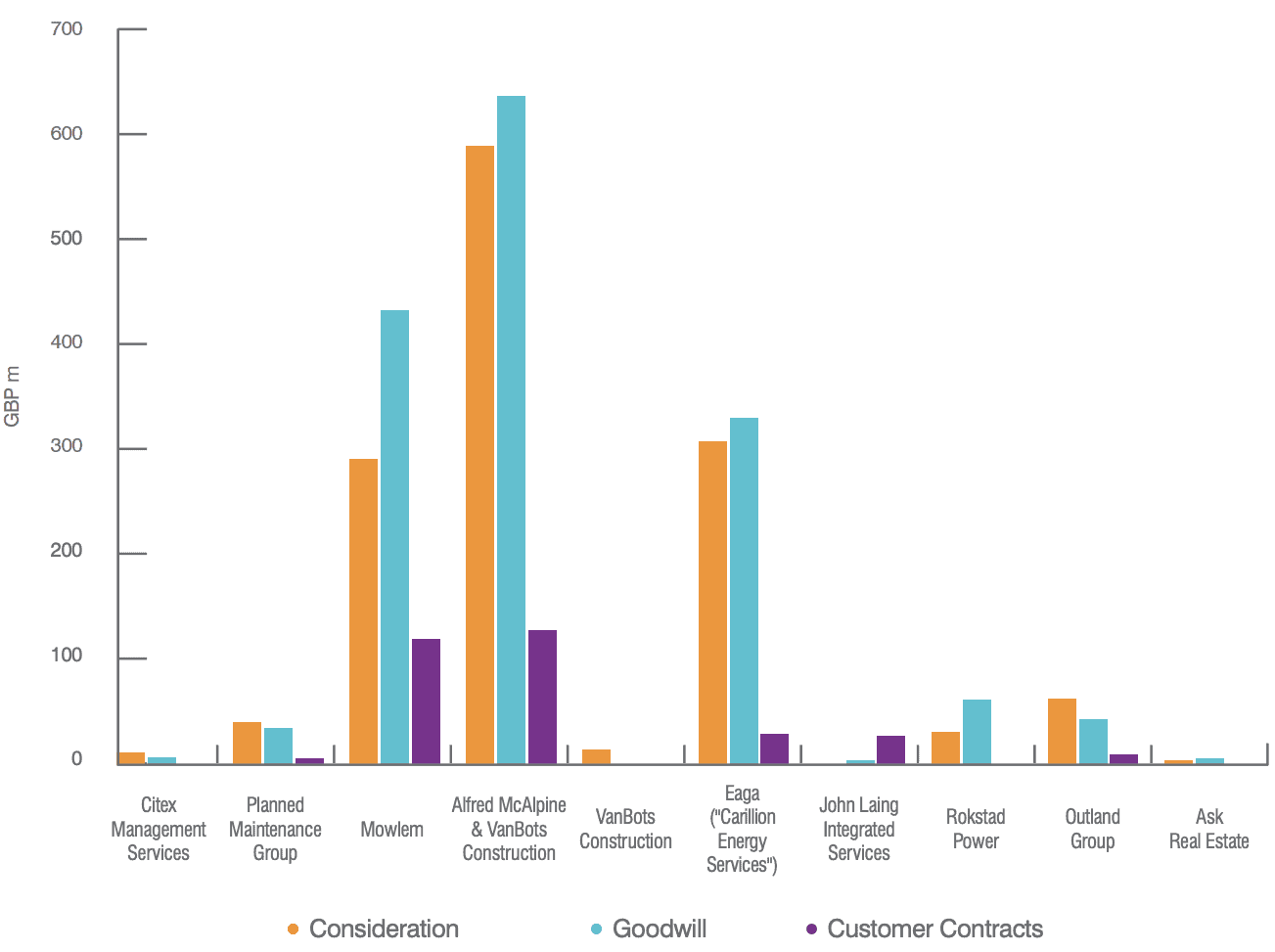

As demonstrated, this was not the case with Carillion. It is reasonable to assume that the original recognition of goodwill was not just representative of synergies. A glance at the FVE details of Carillion’s most recent acquisitions in the above graph demonstrates the exaggerated amount allocated to goodwill.

Carillion managers can be forgiven for overpaying for target companies, as the future is unpredictable. However, in subsequent years, where financial performance did not meet with initial expectations, there should have been impairment to goodwill. The current accounting policy allows goodwill impairment tests to be subjective, and this case study shows that a lack of clarity in the reporting of a business’s assets can obscure the true performance of that business, exposing investors to risk that need not be inevitable.

Who’s Next?

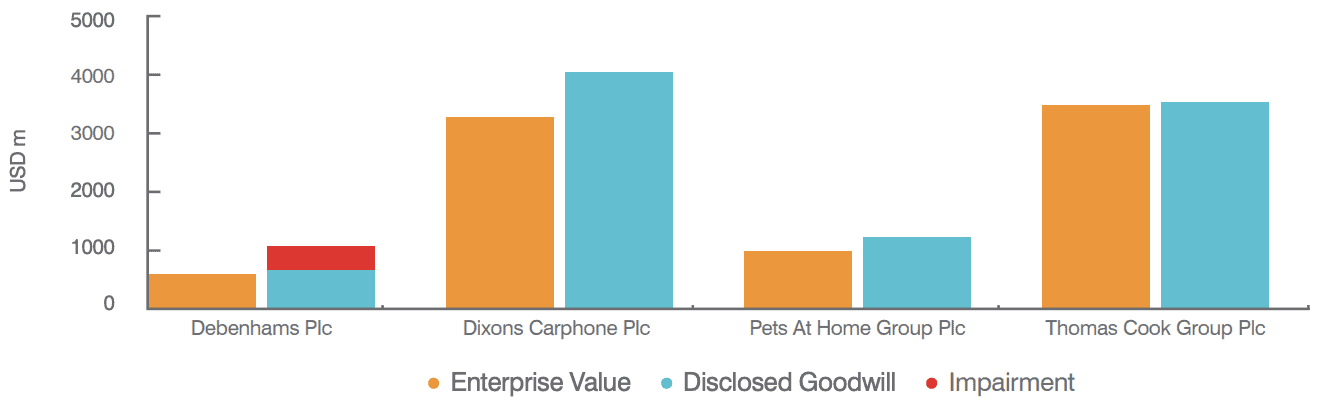

Of course, Carillion is not alone. The graph below shows a handful of UK-based companies with goodwill exceeding market enterprise value in 2017.

Following the completion of our analysis, the new finance director of Debenham’s took a decisive impairment against goodwill, lowering the carrying amount by almost $400m, resulting in cancelled dividends and a pre-tax loss of over $600m. 92 planned store closures at Dixons, upward pressure on payroll costs at Pets at Home, and the recent 25% plunge in shares at Thomas Cook; 2018 has been a tough year so far for these companies too.

As evidenced by disproportionately high levels of goodwill booked for 2017, management expected higher earnings than the market did. In fact, investors do not seem convinced that high levels of goodwill suggest higher future earnings. On the contrary, there is a vast body of research that shows where Goodwill announced following FVE is higher than expected, market participants react negatively.

This implies two things; firstly, that investors are not fooled by high levels of goodwill; they recognise it may mean management overpaid for an acquisition. Secondly, it demonstrates that information provided through FVE disclosure is used by investors. In line with the FASB objectives, if financial information is used, it must be useful. To be useful, these FVE disclosures must be accurate.

Read the 2019 Analysis: Goodwill Hunting: How Not to Miss the Mark in Financial Accounting

There are many valuable learnings from the collapse of Carillion. We see the improper accounting treatment of intangible assets as the most critical. In an increasingly intangible global economy, it is vital that the financial reporting standards keep up with the tide. Ensuring that post-acquisition FVE information is based on objective, accurate valuations will help with corporate transparency, reduce risk, and boost investor confidence. Assuming this will result in lower levels of disclosed goodwill, this will help to reduce the impact of management reluctance to impair.

Logically, it would make sense for intangible valuations to be conducted pre-acquisition too, to assist with corporate governance, reduce the occurrence of reckless M&A, and lower the risk of subsequent corporate collapse. In an age where confidence in audit quality is waning, higher standards for FVE accounting are vital.